CalPERS’ recent announcement that it was cutting back on its investment in commercial real estate by up to $3 billion was the equivalent of a big sneeze heard across the commercial real estate world, setting off industry fears that other pension funds might catch CalPERS’ cold… or worse.

As the country’s largest public pension fund, the California Public Employees Retirement System—and the decisions it makes—matters to markets, especially following on the heels of GE Capital’s own inoculation against real estate through the sell-off of most of its property investments. Clarifying whether there’s a real risk of contagion starts with a diagnosis of the nature of the steps CalPERS is taking to get healthy, as well as recognition that CalPERS is likely to remain quite active in real estate even following these steps.

CalPERS is not exactly underexposed to real estate. It currently has $25.5 billion in real estate assets, approximately 8 percent of its more than $301 billion in total assets. This represents a sharp recovery for the pension fund. During the credit crunch, CalPERS’ assets plunged to $164.7 billion from a pre-crisis high of $260 billion, with the mortgage meltdown and larger financial crisis wiping out nearly half the value of its real estate portfolio alone.

So what are the properties that might get sold off, as the first move under the pension giant’s plan to halve the number of its external money managers by 2020?

So what are the properties that might get sold off, as the first move under the pension giant’s plan to halve the number of its external money managers by 2020?

Well, CalPERS has said it plans to sell non-residential legacy assets, either individually or as a unit, and re-invest the proceeds in other real estate properties that it says "are more aligned with our current strategy." The $6 billion legacy property portfolio includes about 80 funds.

Let’s take a look at one fund that CalPERS defines as a legacy partner in its 2013 CIO performance report: TPG Hospitality Investments IV, a joint venture created in 2006 with the Procaccianti Group.

TPG properties include the Westin Fort Lauderdale, a 293-room Florida hotel that barely escaped foreclosure earlier this year, and the St. Louis Marriott West. The St. Louis hotel was purchased in 2007 with a $39.7 million loan from Wachovia Bank, according to CrediFi data.

The Marriott loan matures in March of 2017 and has monthly interest payments of $192,357, at a 6 percent interest rate; about $38 million of the principal remains. The maturity date for the Westin hotel loan was reportedly pushed off during foreclosure proceedings by two years, until 2019.

Other managers associated with the legacy portfolio include Starwood Capital and CBRE Global Investors. Blackstone's Park Hill Group is handling the divestment and plans to have a deal completed by the end of this year, CalPERS says.

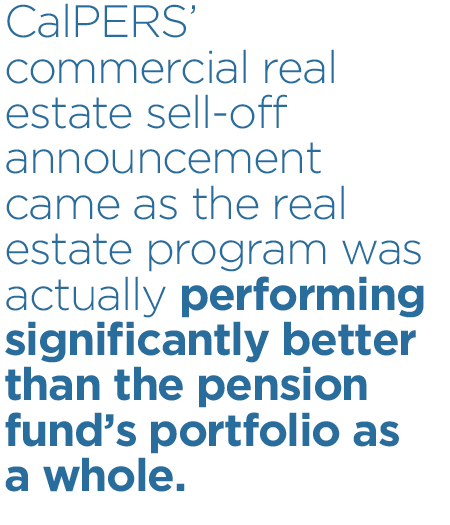

CalPERS’ commercial real estate sell-off announcement came as the real estate program was actually performing significantly better than the pension fund’s portfolio as a whole. Whereas CalPERS reported a preliminary 2.4 percent net return on investments for the 2015 fiscal year—just short of its 2.5 percent goal for this year and down from 18.4 percent in 2014—its real estate portfolio returned about 13.5 percent. Yet when compared to long-term goals, the real estate program has fallen short of its 10-year goal by 7.9 percent and its five- and 20-year goals by approximately 3 percent, the Wall Street Journal reported in June.

The problem appears to be not with real estate as a class, but with the legacy investments that no longer fit into CalPERS’ current strategy.

Recent investments that appear to reflect that strategy include technology properties such as those purchased by TechCore, a joint venture with GI Partners that over the past two years has acquired properties including the 30-story Los Angeles telecom hub One Wilshire and the Raytheon and DirecTV buildings on East Imperial Highway in El Segundo, Calif.

Loans totaling about $150 million for both acquisitions are in the same CMBS deal, with both originating in August of 2013 and maturing in August of 2023. Interest payments for both come to a total of $577,164.

It is worth noting that while the TechCore investments appear to reflect a current interest in technology properties, GI Partners also runs two of the funds CalPERS classifies as legacy partners.

How contagious is this cold then? Though it’s not entirely clear just how the $3 billion real estate sell-off will play out, CalPERS is neither sitting around with a handkerchief nor having radical treatments. Rather, the institution is taking older properties out of its legacy portfolio and investing in funds that look more promising, effectively drinking lots of tea with honey—doing what it can to get stronger, fast. Whether other pension funds will catch CalPERS’ cold, though, remains to be seen.

Ely Razin is CEO of CrediFi, a big data platform serving the commercial real estate finance market. He can be reached at [email protected].

Ely Razin is CEO of CrediFi, a big data platform serving the commercial real estate finance market. He can be reached at [email protected].