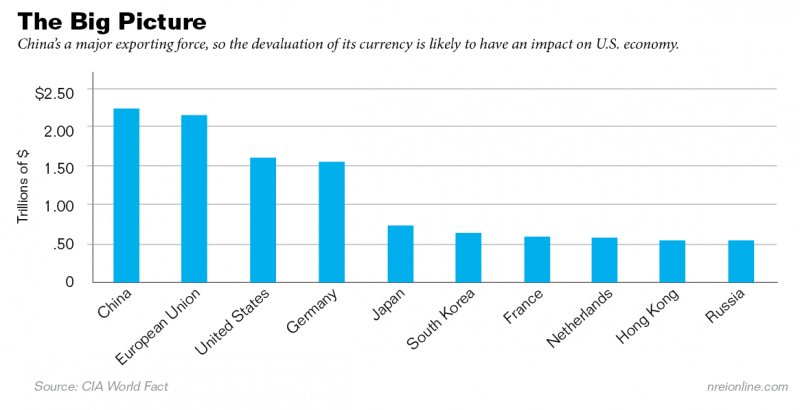

China’s surprise currency devaluation this week could be a net positive for U.S. commercial real estate capital flows and cap rates, but a mixed bag for the U.S. economy.

When the world’s second largest economy and largest exporter surprises investors with an overnight currency devaluation, investors are likely to increasingly seek out safe-haven assets, including U.S. real estate. The surprise move by the Chinese monetary authorities should increase real estate’s status as a “most favored” asset class as investors seek out stability in a time of greater uncertainty. As it relates specifically to Chinese capital flows, if the PBOC allows its currency to decline precipitously, we don't know whether Chinese investors will be priced out of the U.S. real estate market or if it will actually lead to an increase in Chinese capital flows as they seek refuge from a free-falling currency. In addition, U.S. Treasuries should see increased popularity, resulting in reduced Treasury rates and sustaining today’s low yield environment.

Declining Treasury rates will provide further support for stable to even declining cap rates, as capital seeking stable yields flows increasingly to real estate, resulting in additional support for future real estate values. In times of uncertainty and low yields, commercial real estate is increasingly favored among investors.

However, the impact of a depreciating yuan on U.S. economic growth and demand for real estate space is likely to be decidedly mixed. Domestic economic growth will face increased headwinds as exports are placed at an increasing disadvantage, in an environment already challenging for U.S. goods overseas.

How much of an impact this will have depends both on how much the yuan is overvalued and, just as important, how much the PBOC allows the yuan to depreciate. While increasing imports are a negative for economic growth, they are a positive for West Coast industrial space demand, as imported goods from the Asia Pacific region are likely to fill up warehouses from Seattle to San Diego. On the other hand, luxury retail could suffer if the yuan depreciates significantly against the U.S. dollar and Chinese economic growth slows precipitously.

Chinese currency devaluation will serve to reduce inflation in the U.S., as China exports its deflation. This will have two effects. First, it will reduce pressure on the Fed to raise rates and, as we move further away from achieving 2 percent inflation, caution at the Fed will benefit companies through continued low cost of capital. Second, a depreciating yuan increases U.S. consumer purchasing power. How much of an impact this will have depends on how much consumers actually increase their spending and how much is spent on domestic versus imported goods. The consumer’s propensity to exercise increased purchasing power may be tempered in the short-term by negative headlines relating to Chinese economic instability.

Overall, real estate should be a net beneficiary of the depreciating yuan if investors are increasingly drawn to the asset class, providing additional pricing support. The downward pressure exerted on Treasury rates will further support future pricing as the reference rate should remain stable or even decline further.

Christopher Macke is director of research and investment strategy at American Realty Advisors.