Pension funds, life insurance companies and private equity funds have been focused almost exclusively on purchasing core properties in a handful of top markets. That tunnel vision may start to expand in 2012 as institutions prepare to venture further out on the risk spectrum.

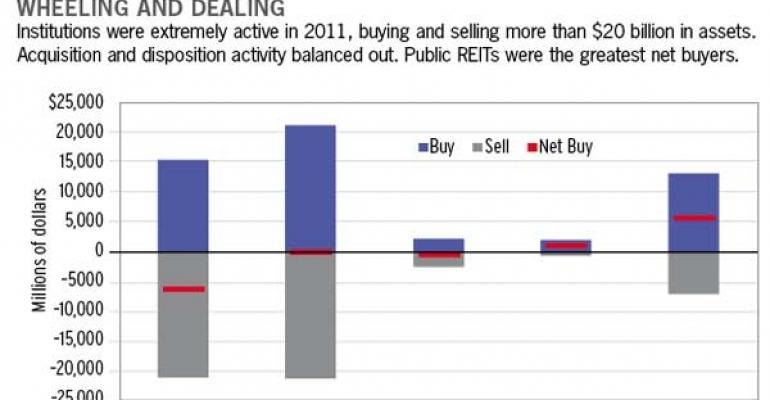

Institutional investors have plenty of capital to spend. In fact, institutions have been among the most active buyers in the market by dollar volume. For example, institutions outspent both REITs and private buyers for office properties in 2011, and acquired $21 billion of the $52.6 billion in office properties that were sold last year, according to the CoStar Group.

The bulk of that institutional capital is flowing to the same places—premium properties in markets such as New York, San Francisco and Chicago. Those core transactions have played a key role in kick-starting sales activity in the wake of the global financial crisis. The voracious appetite and limited supply also has created bidding wars that have sent prices soaring to levels reminiscent of the peak of the market in 2006 and 2007. For example, UBS Realty Investors recently purchased Exchange Place in Boston for $610 million, or about $510 per sq. ft.

Despite the escalating prices, the majority of institutions are still focused on the relative safety of buying low-risk properties in major metros. That trend may not be as significant as it was in 2011, but it clearly is continuing in 2012. A large percentage of institutions don’t want to stray too far from gateway markets such as New York, Washington D.C., Boston, San Francisco, Los Angeles and, increasingly, Seattle for office and multifamily, as well as markets such as California’s Inland Empire for industrial.

“I think there is still a very strong risk-management culture, risk-controlled approach that investors are taking,” says Patrick Halter, CEO of Principal Real Estate Investors in Des Moines, Iowa. “Investors are applying those lessons learned in the last cycle, and at this stage in the recovery, they are not making mistakes,” he says.

That conservative strategy remains fairly well entrenched across the spectrum of both domestic and foreign institutions. However, while institutions are still proceeding cautiously, they are also starting to take incremental steps toward more value-add opportunities. “We spent most of 2008 and 2009 curled up in a ball, hoping. Now we are slowly coming out of that defensive crouch position,” says Jeffrey Havsy, director of research at the National Council of Real Estate Investment Fiduciaries (NCREIF) in Chicago.

Ready for risk?

The expectation for 2012 is that as institutions gain more confidence in the economic recovery, then they will be willing to take on more risk. “We fully anticipate that happening, and we hope that we got out in front of that a little bit in 2012,” says Len O’Donnell, president and chief operating officer of San Antonio-based USAA Real Estate Co. “We went out to Houston and some other markets, and I think we got some really good buys.”

For example, USAA Real Estate acquired a preferred equity interest in the Hilton Garden Inn, a 190-unit hotel located in Houston’s Energy Corridor. The firm acquired the property as part of its involvement in the Admiral Capital Real Estate Fund.

“Barring another economic downturn, the worst in the cycle is absolutely statistically behind us,” says David Gilbert, chief investment officer at New York-based Clarion Partners. Vacancy rates and absorption numbers show signs of improvement across most property types, and rents appear to be stabilizing. Although some markets are still experiencing very anemic growth, other markets such as Silicon Valley and Austin are surging ahead with their recovery.

In addition, the work that institutions and funds have put into rebalancing portfolios to include less leverage and more high-quality properties is providing added confidence to take on slightly more risk—particularly as buyers search for higher returns. Clarion Partners certainly falls into that category. “We believe that value-add investments actually compare favorably now, in large part because there is so much capital seeking investment in a relatively narrow set of really, really high-quality core markets,” says Gilbert.

Apartments, for example, have been a top pick for institutional investors, thanks to strong fundamentals in that sector. However, the lack of supply and heightened demand is sending prices soaring. The average cap rate on mid-rise apartments dropped to 5.7 percent in fourth quarter, rivaling the pricing that was occurring in 2005 and 2006 when cap rates averaged between 5.1 and 6.2 percent, according to New York-based Real Capital Analytics.

Escalating prices and lack of supply of quality for-sale properties is prompting institutions to explore opportunities in secondary markets and new development as they search for higher yields. “Like a lot of our counterparts, where we are seeing the biggest interest is in multifamily investments,” says Gilbert.

That is no surprise, considering that apartments have been generating the highest returns recently. Apartments out-performed all other sectors in the NCREIF Property Index in 2011 (NPI) with a return of 15.5 percent. That rate even exceeded the gain for S&P 500, which returned over 11 percent.

For example, Clarion Partners has entered into a joint venture with The Residential Group LLC to develop The Crest at Brier Creek, a 291-unit upscale garden apartment community in Raleigh, N.C. The firm also has apartment developments underway or planned in key markets, including Manhattan, Boston, San Diego, Southern Florida and, potentially, Denver.

“The amount of capital flowing into the sector has resulted in a situation where even the stabilized cash-flow return from building new product is superior to that from buying existing product or property,” Gilbert says. Clarion Partners has been finding opportunities to develop new apartments where the initial return upon stabilization of a newly built property is projected to be 75 to 100 basis points higher than buying an existing stabilized property.

Buyers tap breaks

It appeared as though the flight to safety that occurred in the wake of the economic crisis was beginning to loosen during early 2011. Institutions started to move out to secondary markets, and less than stellar assets in core cities as the economy started to improve and the commercial real estate markets continued to stabilize.

However, that activity stalled when the European credit crisis reignited. Sales velocity that had jumped from $35.1 billion in the first quarter to $60.5 billion in the second quarter pulled back to $54 billion in the third quarter, according to RCA.

“Investors were looking to wait out the volatility to see what was going to happen before committing a whole lot more capital,” says Greg MacKinnon, Director of Research at Pension Real Estate Association in Hartford, Conn. Buyers remained active in the fourth quarter with some large core sales helping to elevate sales volume to $61.6 billion. However, the caution that resurfaced in the latter half of 2011 has carried over into 2012.

Institutions are watching to see what happens with the European debt crisis, the U.S. economy and job growth, the presidential election and the availability of debt financing. “It is almost like we are back where we were in early 2011 in the sense that the capital that is being committed is going to the major markets and the high-quality properties,” says MacKinnon. “There are not a lot of commitments yet, because people are waiting to see what is going to happen with a lot of these macroeconomic events,” he adds.

Moving towards value-add

Institutions are moving, albeit cautiously, into more value-add situations. For example, buyers are considering buildings with leasing risk or shorter-term leases. Although apartment development is by far the most active sector, investors are beginning to show interest in office and industrial build-to-suit projects that are leased to solid corporate or government tenants. Institutions also appear more receptive to non-core property types such as medical office, senior housing, student housing and self-storage. “Those property types continue to attract interest, and we will probably see increases in activity in those sectors over the next year,” adds Havsy.

Another component to the value-add shift is that investors are finally beginning to migrate from gateway cities like New York; Washington, D.C.; San Francisco and Los Angeles to secondary markets, such as Houston, Atlanta, Denver and Seattle. According to RCA, Manhattan, Los Angeles and Chicago have consistently ranked as the top markets for sales volume for the last four years running. However, activity has picked up considerably in the past year in secondary markets. Atlanta, for example, jumped from 15th to ninth place in 2011 with $64.9 billion in total sales, according to RCA.

“There clearly is a much broader landscape of areas that the institutional investment community is willing to invest in now, and we think that is going to continue to be the case as we go into 2012,” says Halter. For example, Principal purchased an empty 500,000-sq.-ft. office building in northwestern Houston last year. “We were confident that, from a leasing and asset management perspective, we could take the empty property and lease it up and bring it to a core level,” he says. Principal recently signed a lease with a tenant who has committed to fully occupy the building.

The tolerance to risk varies, depending on the individual investor. “We are not shifting to secondary markets in search of higher yield. We are just not comfortable with the longer-term economic outlook for a lot of those markets,” says Gilbert.

However, Clarion Partners is willing to take on more risk within those core markets. For example, Clarion recently committed to buy a CBD office building in Seattle that will be vacated by the existing tenant. The company went into the sale with a tenant in hand that agreed to lease the majority of the building, and Clarion will close the property with a signed lease that will take the building to 90 percent occupancy in the near future.

One way that institutions are mitigating that risk is by forming joint ventures with equity partners who also manage and operate the assets. For example, Faris Lee represented the seller in the sale of the District at Green Valley Ranch, a 384,107-sq.-ft. community retail center in Henderson, Nev. Vestar Development purchased the property in a joint venture with New York-based Rockwood Capital for $79.3 million. “That is a deal where we saw a tremendous amount of activity, because of the scale of the deal,” says Richard Walter, president of Faris Lee Investments in Irvine, Calif. “It had some issues with it, but for the right operator, there was a good value-add component to it.”

Weighing risk vs. return

The common thread for many institutions—whether they are looking at core, value-add or opportunistic strategies, or a combination of all three—is that there is still plenty of capital to spend and institutions want to put that money to work in commercial real estate.

“Particularly in this environment of slow growth and low yields, we are seeing that core real estate is very attractive to a lot of investors, both domestically and from around the world,” says Steve Corkin, a managing director and head of Investor Relations at AEW Capital Management in Boston.

AEW also is active across the risk spectrum in value-add and opportunistic investments. Among the $2 billion in domestic acquisitions AEW made in 2011, the acquisitions were fairly evenly split between core and value-add/opportunistic properties.

The low-interest rate environment and low returns found in other investment alternatives such as corporate bonds or treasuries will continue to fuel investor appetites for low-risk core real estate investments.

There are plenty of institutions that will continue to buy core or nothing at all. Other buyers will try to find ways to improve yield, whether that means pushing out geographically into secondary markets that have class-A properties in them, or going in the other direction by buying class-B properties in a class-A location and having an operator that can improve on that.

The intense competition for low-risk property has produced prices that are at, or even above, the pricing that occurred at the peak of the market in 2006 and 2007. The investment landscape shifted again recently with the Fed announcement that it would keep interest rates near zero until 2014 as opposed to 2013 as what was previously stated. “I do believe that is going to put more pressure on property yields to move down further,” says Corkin. “I wouldn’t be surprised if we saw another 25 to 50 basis points of compression on average in the next year because of that.”

The NCREIF Index reported 2011 returns that were nearly 15 percent on core properties. About 5 to 6 percent of that return was income, while the remaining 9 to 10 percent was in appreciation. The consensus is that while there will still be some appreciation in the short-term, it most likely will not be as high as what was achieved in 2010 and 2011.

Investors are willing to accept lower returns in exchange for the safety that core assets often provide in terms of preservation of capital and a steady income from high occupancies. The historically low-interest rate environment also has made those returns more palatable. The end result is that the unlevered core returns of 7 to 8 percent that many institutions are able to achieve still compare favorably to alternative investments. “Other investors want a little bit of a higher return, which is why they are going into the value-add space,” says Halter.

The returns on value-add properties are generally producing a 10 to 15 percent return. Investors that are moving farther along the risk spectrum to opportunistic properties that have more significant challenges generally have return thresholds of 17 to 20 percent. “That is the profile of what investors want to achieve as they think about going up the risk spectrum,” he says.

Sidebar: Capital Solutions

Despite the steady stream of capital returning to the commercial real estate marketplace, accessing funds to buy new and refinance existing property remains a challenge for many borrowers. But institutions are finding opportunities to fill that void and generate some attractive returns in the process.

Life insurance companies, pension fund managers and private equity groups are stepping up to provide debt and equity capital for cash-strapped borrowers. “We have all been waiting for the surge in distressed opportunities, but I think this year we are going to see more opportunities in consolidating debt and acquiring distressed debt,” says Len O’Donnell, president and chief operating officer of San Antonio-based USAA Real Estate Co.

There is still a considerable amount of new capital that needs to be brought to the real estate market to help bail-out borrowers and properties that are in dire need of fresh financing. In addition, many of the properties that were acquired in 2007 with five-year loans are now facing refinancing at lower values or more conservative underwriting. Owners that have been struggling to hang onto properties until the recovery are simply running out of time, and money, in the slow recovery.

Case in point is the sizable volume of loans set to mature over the next four years. For example, about 10 percent or $150.6 billion in commercial and multifamily mortgages held by non-bank lenders and investors will mature in 2012 alone, according to a recent survey by the Mortgage Bankers Association (MBA). That figure does not include data from banks and thrifts, which currently hold $793 billion in mortgages for income-producing properties.

“I think we will see a shift in 2012 where a lot of institutional investors are going to be an active provider of credit and debt, and start to fill the void where a lot of traditional lenders are not able to deliver the market liquidity needed for the refinancings,” says Josh Cleveland, a partner at Clairvue Capital Partners in New York.

Fresh capital fix

Many ownership groups that bought property at peak prices are under financial stress because of the need to lower the leverage on a property or perhaps restructure the existing ownership group. However, the underlying properties are good quality assets.

Established in early 2010, Clairvue Capital Partners is a real estate private equity fund manager focused on investing in recapitalizations and secondary purchases in the private equity real estate sector. Clairvue provides the necessary capital to help owners pay off maturing debt, as well as cover leasing costs and capital expenditures. “We are finding a tremendous amount of opportunity looking at good management teams, and bringing them the capital to stabilize their portfolios,” says Cleveland.

Clairvue Capital raised $250 million during the first half of 2010 to create its Clairvue Capital Partners I, a fund with targeted returns of 16 to 20 percent. The fund originally had a four-year investment target, but has deployed 80 percent of its money in 18 months. “What that specifically points to is the demand for specific types of capital,” says Cleveland. “To be able to deliver equity in this marketplace and still approach it as a partnership with ownership, as opposed to being predatory or confrontational to the existing owners, has proven to be a strategy that is well received by the marketplace.”

For example, Clairvue Capital I acquired a secondary interest in the Buchanan Fund V last fall. Essentially, Clairvue acquired the $25 million original investment of an unnamed institution that was looking to exit the fund. Buchanan V originally raised over $400 million that was invested in office, retail, multifamily and industrial equity as well as first mortgage and mezzanine debt investments in markets predominantly in the Western U.S.

Clairvue Capital is planning to launch its Clairvue Capital Partners II in 2012 with a target equity raise of $500 million.

Principal Real Estate Investors is one life insurance company that has taken the lead in meeting the growing demand for mezzanine capital. The firm provided about $300 million in mezzanine financing in 2011. “There is a real interesting opportunity to provide capital—filling the gap between the 65 percent to 75 percent loan-to-value range,” says Patrick Halter, CEO of Principal Real Estate Investors in Des Moines, Iowa. “That type of capital produces an 8 to 9 percent return, which fits very, very well with what a lot of equity capital sources are looking for.”

The industry-wide shift to provide lower leverage loans has created more demand for capital to bridge the gap between the primary loan and the equity piece. “That is going to be the most inefficient part of the market moving forward, and on a risk-adjusted basis, I think we will be able to capture some very attractive returns,” says O’Donnell.