The leading providers of capital for multifamily loans are still on shaky ground—years after the financial crisis ended.

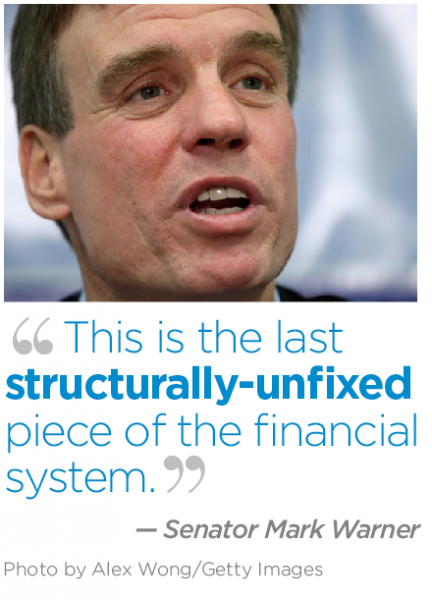

“This is the last structurally-unfixed piece of the financial system,” said U.S. Senator Mark Warner (D-Vir.), ranking member of the Senate Securities, Insurance, and Investment Banking Subcommittee, at an October 6 presentation on Fannie Mae and Freddie Mac at the Bipartisan Policy Center.

The last attempt to reform Fannie Mae and Freddie Mac died in Congress after the 2014 elections. The mortgage giants continue to provide trillions of dollars in capital to the housing market, even though their future is uncertain. The Corker-Warner reform proposal, co-authored by Sen. Warner, provides a possible template for reform, but Congress is unlikely to act on it before the Presidential election next year. In the meantime, the housing finance system, a huge piece of the U.S. economy, remains vulnerable.

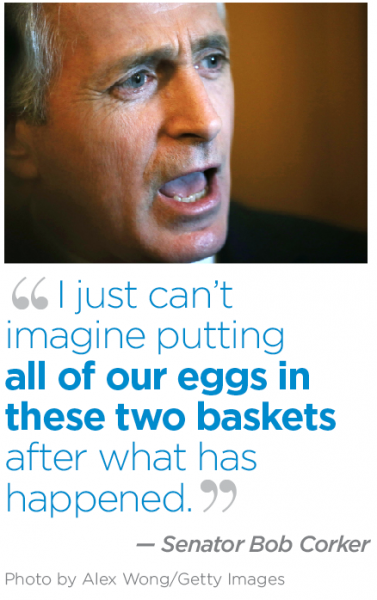

“I just can’t imagine putting all of our eggs in these two baskets after what has happened,” said U.S. Senator Bob Corker (R-Tenn.), member of the Senate Banking Committee and co-author of Corker-Warner.

“Bigger and badder” than ever

These two gigantic agencies provide the capital for many multifamily mortgages and the vast majority of U.S. home loans. The government seized them during the financial crisis and has run them ever since under the oversight of the Federal Housing Finance Agency (FHFA). Investors still buy and sell stock in Fannie Mae and Freddie Mac, though the shares are probably worthless and trade at a tiny fraction of their old values. In the meantime, the companies transact trillions of dollars in business and have returned hundreds of billions of dollars in profits to the federal government.

However, Fannie Mae and Freddie Mac are still two giant accidents waiting to happen, according to a new book by the journalist who exposed the troubles at Enron, Bethany McLean. “Bigger and badder than ever,” she says.

However, Fannie Mae and Freddie Mac are still two giant accidents waiting to happen, according to a new book by the journalist who exposed the troubles at Enron, Bethany McLean. “Bigger and badder than ever,” she says.

The biggest risk is that Fannie Mae and Freddie Mac currently operate without any reserves—even though they issue mortgage bonds and guarantee that many bond buyers will get their money back, no matter what happens to the underlying loans.

“I still have a fear that we could end up with a down quarter, where you could have all hell break loose,” says Warner. “You see some of the entities get close in a down quarter and not having any reserves to draw upon.”

If Fannie and Freddie needed money, Congress would have to authorize the payment. Even a relatively small amount—a few hundred million dollars—would likely trigger an enraged discussion.

The Corker-Warner model

The Corker-Warner bill provides a template for bi-partisan reform of the GSEs—turning them back into private companies that provide money for home loans and multifamily mortgages. They would raise that money by selling bonds guaranteed by the federal government. Without a guarantee, it’s impossible to imagine Wall Street bond investors contributing cash to fund 30-year home loans. During the financial crisis, bond buyers refused to buy even privately-issued commercial mortgaged-backed securities backed by 10-year loans.

“The centerpiece of this new system is an explicit and limited government guarantee on certain kinds of single-family and multifamily mortgages,” according to a description provided by Enterprise Community Partners, Inc. The guarantee would probably be carried out by a government insurance fund. Banks and other lenders could make loans that would meet the standards set by the fund. The privatized Fannie Mae, Freddie Mac and their competitors would buy the loans and issue mortgage bonds guaranteed by the insurance fund.

“The centerpiece of this new system is an explicit and limited government guarantee on certain kinds of single-family and multifamily mortgages,” according to a description provided by Enterprise Community Partners, Inc. The guarantee would probably be carried out by a government insurance fund. Banks and other lenders could make loans that would meet the standards set by the fund. The privatized Fannie Mae, Freddie Mac and their competitors would buy the loans and issue mortgage bonds guaranteed by the insurance fund.

That might leaves taxpayers on the hook for potential losses if enough loans fail, but the proposed guarantee would have clear limits. The mortgage would only cover 80 percent of the value of the property, so the first 20 percent of losses would strike the owner’s equity. The next 10-to-15 percent of losses would strike B-piece bond investors. The next 10 percent of losses would strikes that lender’s risk-based capital. The next 5 percent would hit the insurance fund, according to finance experts from the National Multifamily Housing Council. So a foreclosed property would have to lose half its value before any taxpayer money was at risk.

Some conservatives in Congress feel even that limited guarantee is too much.

“There is a very strong feeling, especially in the House [of Representatives], that we need to get the government completely out of the business of a backstop guarantee,” says Warner.

And some progressives also resist reform. “Progressives felt that the status quo, even as flawed as it was, was better than the potential of the kind of changes we were thinking of,” says Warner.

The current system is vulnerable, however. A proposal by in the House of Representatives by Jeb Hensarling (R-Texas) would effectively wipe out Fannie and Freddie altogether.

“The status quo is fine until it’s not,” says Warner. “If there is a sudden move in the House to get rid of any government backstop, if Mr. Hensarling’s bill becomes law… You talk about disruption....”