In its second-quarter performance results announced Aug. 17, Staples reinforced the idea that one way or another, it was determined to implement positive and lasting operational changes.

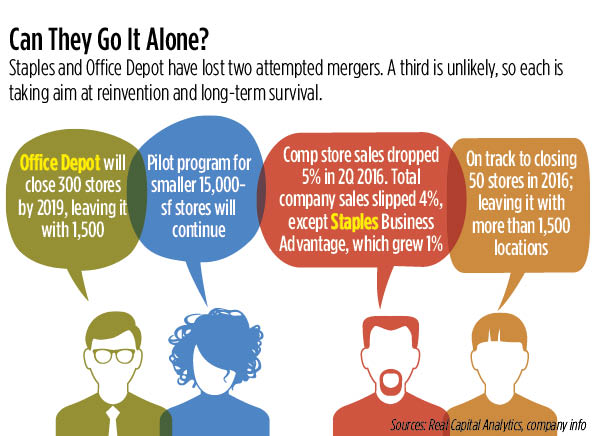

Staples closed five stores during the period, part of its plans to shutter 50 stores in North America this year. It also reported an increase in sales from Business Advantage, its contract business that sells office supplies and technology products to businesses and institutions.

It is Plan B for Staples. For most of 2015 and the first quarter of 2016, the Framingham, Mass.-based retailer tried to acquire rival Office Depot. It was a bid to create a company that could respond to relentless price constraints, the commodity status of most in-store products, and American workplaces reducing their use of traditional office supplies.

Yet in May the U.S. District Court in Washington, D.C., affirmed the Federal Trade Commission’s earlier ruling to block the acquisition. Federal authorities were wary that a combination would create a burdensome monopoly, harming consumers.

Industry analysts remain incredulous at the federal court’s decision.

“The antitrust court was absolutely wrong,” says Daniel Binder, a managing director and senior equity research analyst at Jefferies & Company. “I’m shocked that they are worried about JPMorgan having a hard time buying pencils. Somehow, a monopoly will take advantage of Fortune 500 companies?”

Rejection is rarely easy to accept. Yet Staples, and Office Depot for that matter, must now chart different courses for, hopefully, more successful futures. The question is: What will that future look like?

In the period before the acquisition plan was announced, Office Depot and Staples saw combined cap rates that were increasing relative to power centers and other big-box retail tenants, according to research from Real Capital Analytics. At the time, cap rates ranged from 7.7 percent to 8.0 percent. After the announcement, investors bid rates down to to 7.1 percent in the second quarter, when the deal was called off.

“With uncertainty around some of these tenancies, will cap rates for these assets start to trend up above the big box and power centers overall again, just as was seen ahead of the merger announcement?” asks Jim Costello, a senior vice president at Real Capital Analytics.

Laying out the challenges

Going it alone will likely entail some turbulence, at least initially. Both companies have planned store closures in an effort to boost the efficiency of their properties. Office Depot recently said that it plans to close an additional 300 stores to the 400 it had previously announced.

“Staples will probably experience a sales transfer of 20 percent,” Binder says. “It has been a critical time for several years, and we’ve seen turnovers in management, failed combinations and other secular headwinds.” In its second quarter results, Office Depot noted that its round of 400 store closures resulted in sales transfers above 30 percent.

Staples is supposedly exploring five-year lease terms on certain properties, instead of the more typical 10- to 15-year terms, a transition that could impact cap rates on property deals.

For landlords, shorter terms confer more flexible timetables for remerchandising and redeveloping spaces, according to Anjee Solanki, the national director of retail services for Colliers, U.S. Although sales activity has not picked up so far in 2016, the triple net group at Colliers inferred that single-tenant Staples could trade between the high-7 percent and low-8 percent range, with an average of about 7.5 percent. Office Depot could trade in the low- to mid-7 percent range, with an estimated 7 percent average.

Office Depot cap rates have the potential to trade a tighter spread than Staples because its properties tend to be absolute triple-net leases, while Staples typically has more double-net leases.

Relocation and reinvention

Expert observations certainly point to a widening of cap rates, given the operational challenges the two companies are likely to face. But that doesn’t mean office supply retailers are adrift without rudders. While stiff headwinds remain for both companies, they can still carve out meaningful successes, Anjee said.

Staples is collaborating with Workbar to offer shared work spaces inside about four select retail locations. The effort will offer high-end workspaces, conference rooms and private phone rooms, among other accommodations.

A number of retailers have already successfully implemented secondary point of service services within their spaces in select locations. JCPenney offers space to Sephora, and Target has partnered for years with Starbucks.

“If a retailer can add a secondary point of purchase,” Anjee says, “it can increase margins on those points of sale by 30 percent to 40 percent.”

Office Depot’s store closures also give the retailer the opportunity to relocate stores to better locations, Anjee notes.