The retail industry is reeling from the persistent announcements of store closures across the United States. The retail sales statistics have been weak and the retail employment losses in March were highlighted in every media outlet. But where have the losses hit more and what can be expected in the next year or so?

When looking at the numbers, the story is not as bad as many have reported. The retail vacancy rate for neighborhood and community shopping centers was flat in the first quarter at 9.9 percent, the same as in the first quarter of 2016. Moreover, rent growth was positive, at 0.3 percent for the quarter. The mall vacancy rate only climbed to 7.9 percent from 7.8 percent at the end of 2016 and rent growth was 0.4 percent during the quarter.

So when and where will we see the impact from the store closures?

First, many of the store announcements have yet to translate into actual closings. Thus, we should see more vacancies in the next three or four quarters. Second, a number of other retailers are expanding into retail space, we are seeing quite a bit of this in the properties we survey. Third, many of the stores closing are in less densely populated or more rural areas beyond the 80 primary metros that we track. Indeed, our tertiary market statistics show an aggregate retail vacancy rate increase to 13.5 percent from 13.2 percent at the end of 2016 and no rent growth.

We are seeing consistent results in the employment numbers. That is, only 14 of 82 primary metros tracked by Reis show a year-over-year loss in retail jobs, but 35 tertiary markets show an employment loss as of the first quarter. It should be noted that nearly all of the retail losses at the national level are in “general merchandise” stores that include department stores as well as supercenters. It should also be noted that the U.S. added retail jobs in April, yet the media stayed mum.

Still, anyone looking at this industry will say the same thing: we are over-retailed. Retail development exploded in the late 1980s through the 1990s. It has subsided in this last cycle as many developers and lenders got burned in the recession. But there are likely still more stores than we need. And with the overwhelming growth in e-commerce we probably need fewer than we currently have in a number of markets. But where to start?

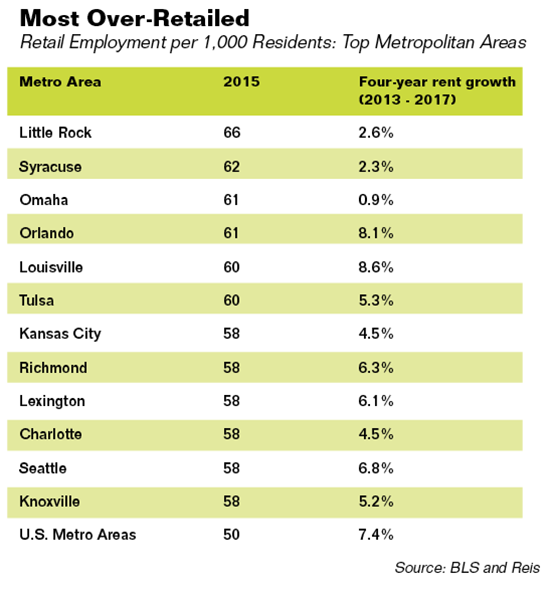

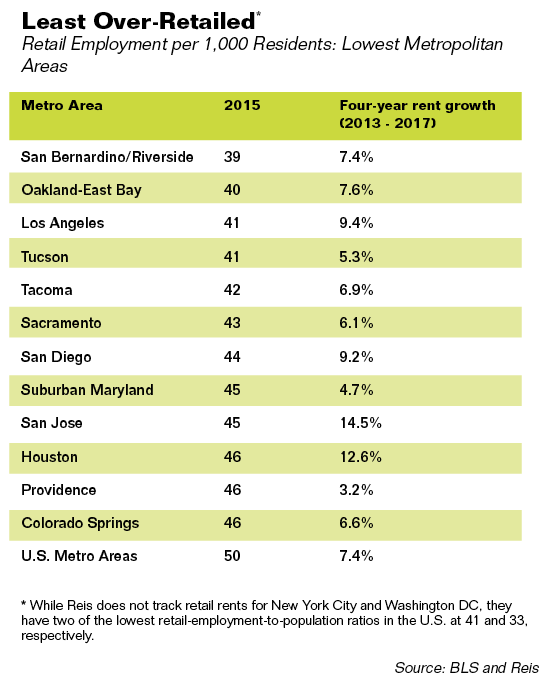

A good way of measuring what markets may be over-retailed is to compare retail employment to population. The table below shows the markets with the highest and lowest ratios of retail employees per 1,000 people and the respective growth in retail rent over the last four years.

As the tables above show, there is a pretty wide gap between the metros that have a high retail employment per population ratio and those that have a low ratio (39 to 66). What’s more significant is the differences in the range of rent growth rates between the top and bottom tables. That is, those with a high ratio had persistently slower rent growth than those with a low ratio. In fact, for the 80 metros tracked by Reis, the correlation coefficient for the four-year retail rent growth and retail employment per 1,000 residents is -22.3 percent. In other words, markets that look to be over-retailed (i.e. with a high retail-employee-to-population ratio) have generally seen lower retail rent growth than those that seem to be relatively under-retailed.

While this correlation coefficient is negative as one would expect, it is still pretty low. This suggests that far more variables are impacting retail rent growth. In fact, the correlation coefficient between population growth and retail rent growth was significantly higher: 42 percent. Thus, population growth drives retail rent growth more than the saturation of the retail industry.

While the numbers show that the retail industry could in fact be over-saturated, the impact of this saturation on the real estate industry may not be as troublesome as many would presume. Again, other businesses are expanding in formerly empty stores, especially non-traditional tenants such as yoga studios and urgent care medical centers. In sum, while the media may overreact to the next jobs report as doom and gloom for the retail industry, it is important to consider what is likely not being reported in the press, which is that the retail industry is performing better than many would assume.

Barbara Byrne Denham serves as an economist and Victor Calanog as chief economist with Reis, Inc, a provider of commercial real estate data and analytics.