Since 2009, traditional real estate investors have had to learn non-traditional ways of buying property in the United States. That is four years of being creative, four years of working with an entirely new breed of seller, four years of learning about foreclosure risk, guarantees, cross-collateralization, forbearance agreements, discounted pay offs, deeds in lieu of foreclosure, which states are judicial vs. non-judicial … the list of new concepts and terminology goes on and on.

It’s hard to imagine such naivety now, but four years ago, observers were talking about a 12- to 18-month downturn. For commercial real estate service providers grounded in bricks and mortar, the industry’s move into non-performing debt investment presented a do-or-die challenge. Many of the brokers who let fear of the unknown hold them back from learning the ins and outs of distressed debt are now behind the curve, or even out of the industry.

For investors and advisors who embraced this new facet of commercial real estate investment, questions beg to be answered. Did we learn these new concepts simply to dig out of a hole, only to relegate debt transactions to the periphery as soon as real estate fundamentals recover? Or is this a new skill set that we should take back to our universities, to prepare the next generation of real estate professionals with the methods we’ve developed and the revelations we’ve come to learn through necessity? In essence, how long will debt take center stage in commercial real estate investing, or has debt gained a permanent and more prominent foothold in the industry?

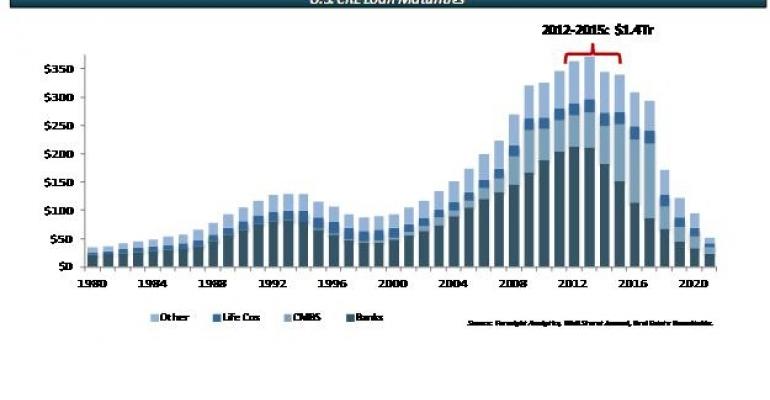

Loan maturities will peak in 2017, which means that from now until then there will be a very real market for non-performing loan sales. Forecasters expect borrowers to struggle to find the ability to refinance themselves to pre-recession values when it comes time to pay back the banks.

Years of Debt Dominance

Today, non-performing loans have become an investment class in their own right. Many first-move investors have already flipped mortgages they bought in 2009 and 2010, recycling those loans to other investors. Banks have also pooled single loans and closed on bulk sales to buyers that know how to slice and dice the portfolios to generate their required initial rate of return before re-distributing portions of those portfolios to other buyers in the market.

Return rates on invested capital are linked to interest rates. In a low-interest-rate environment, investors become satisfied with lower rates of return as long as they are beating the bank. The trillions of dollars that has been waiting on the sidelines for deals that deliver higher returns will likely grow impatient, and appetites for lower returns will grow tremendously.

During New York University Schack’s Capital Markets Conference on Nov. 7, Howard Lutnick, chairman and CEO of Cantor Fitzgerald and BGC Partners, projected that interest rates will stay low for the next few years.

With such a long-term prospect, investors will start accepting lower returns on their capital.

In all likelihood, investors who have been acquiring and restructuring loans based upon an expectation of mid-teen return rates will find buyers willing to accept a lower rate of return from a transaction. The initial investors can then sell those restructured deals at a greater profit while boosting the annual return rate on their initial purchases. This appetite for deals, and increasing competition in the market, is almost sure to fuel transaction volume over the coming years.

Backed by brick and mortar

The other reason that loan sales aren’t going to disappear is because ultimately the price of a loan is determined by the value of the underlying asset. Today, buyers acquire loans at a discount to the unpaid principal balance based on current, depressed asset values. Over time, the loan’s intrinsic value is likely to creep up as real estate values recover. Note buyers who underwrote a 3-year hold period may well see the benefit of putting these loans back into the market earlier than anticipated. By selling, those investors can expect to collect a premium against their original purchase price in addition to achieving a required rate of return, thanks to the likely bounce-back of real estate markets throughout the nation.

Real estate became a financial instrument earlier this century and so it continues to deliver fiscal allure for many investors. As loan holders, investors don’t need to own property any more to make a return on real estate investments; they just need to know how to work the paper. We will see loan sales pushing on for another 8 to 10 years as investors transition from purely bricks–and-mortar plays to being full-fledged participants in the capital markets world.

Andrew Phillips is a managing director for the distressed asset advisory group and national loan sales platform of Newmark Grubb Knight Frank. [email protected]