Data from Trepp LLC showed that CMBS delinquencies decreased in October—the first drop in the monthly delinquency rate in more than a year. The biggest reason for the drop is that loans were liquidated at a more rapid clip during the month. In addition, the Extended Stay Hotels loan, which had been delinquent since late 2009, was finally resolved in October.

Realpoint LLC, the other major research firm that tracks CMBS delinquencies, did not show a decline yet—however its most recent data is through the end of September. In contrast, Trepp’s most recent report runs through the end of October.

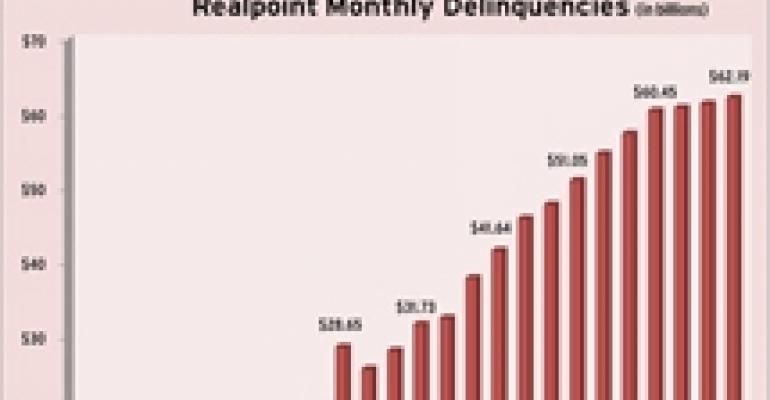

According to Horsham, Pa.-based Realpoint, the delinquent unpaid balance for CMBS rose $801.2 million, up to $62.19 billion from $61.39 billion a month prior. The increase of $801.2 million was greater than the previous two months when delinquencies rose $551.8 million and $387.9 million in August and July, respectively. The growth was still below the average for the first six months of 2010 when delinquencies grew by an average of $3.14 billion per month.

Outside of a slight decrease in both the 30-day and 90+-day categories, the remaining delinquency categories each increased, fueled by further delinquency degradation and credit deterioration. According to Realpoint, “Despite ongoing loan liquidations, modifications and resolutions, the distressed 90+-day, Foreclosure and REO categories as a whole grew by $1.16 billion (2.4 percent) from the previous month after falling for the first time in almost three years from July to August 2010.”

The total unpaid balance for CMBS pools reviewed by Realpoint for the September remittance was $773.61 billion, down slightly from $773.98 billion in August.

The delinquency ratio for September of 8.04 percent (up from the 7.83 percent reported for August) is more than two times the 3.94 percent reported in September 2009 and more than 28 times the Realpoint recorded low point of 0.28 percent in June 2007.

Realpoint maintained its projection for the delinquent unpaid CMBS balance, which it expects to reach between $70 billion and $80 billion by the end of 2010. The firm also projects the delinquency percentage to reach between 8 percent and 9 percent by the end of the year.

By property type, in September, multifamily loans topped retail loans as the greatest contributor to overall CMBS delinquency for the fourth straight month. Retail loans had been the greatest contributor for six straight months prior to June. Delinquent multifamily loans account for 1.99 percent of the CMBS universe and 24.7 percent of total delinquency. The retail default rate increased slightly to 6.8 percent, up from 6.4 percent in August and up from 4.2 percent one year ago.

In its monthly report, Realpoint wrote, “Despite a leveling off over the past five months, we still consider retail delinquency a legitimate concern for the remainder of 2010 and into 2011. A prolonged economic recovery could have further impact on consumer spending and cause retailers to continue to struggle. We also cannot rule out additional store consolidation, closings and potential bankruptcies along with growing balloon maturity default risk as retail collateral continues to suffer from the experienced decline.”

Meanwhile, in its monthly report, New York City-based Trepp said that the CMBS delinquency rate declined to 8.58 percent off of a record high of 9.05 percent in September. It was the first drop in the monthly delinquency rate Trepp reported since July 2009.

According to Trepp, “The bottom line is that as long as the volume of loan modifications and liquidations remains elevated there will continue to be downward pressure on the delinquency rate.”

The delinquency rate one year ago was 4.80 percent. The 30+ day delinquency rate on retail rose slightly to 7.17 percent from 7.13 percent in October.

The delinquency rate on lodging experienced the greatest decline—from 19.33 percent in September to 14.92 percent in October. The delinquency rate for industrial properties fell from 6.48 percent to 6.27 percent. It rose for office properties from 6.62 percent to 6.68 percent and roes for multifamily from 14.43 percent to 14.63 percent.