The vastly different lending practices by lenders on commercial real estate during the boom years are now manifesting themselves in widening delinquency rates.

In the run-up to the market’s peak, aggressive conduit lenders, in an effort to gain market share, offered the easiest lending conditions marked by high loan-to-value ratios and generous underwriting assumptions for increasing values and rents. In addition, they lent to all comers.

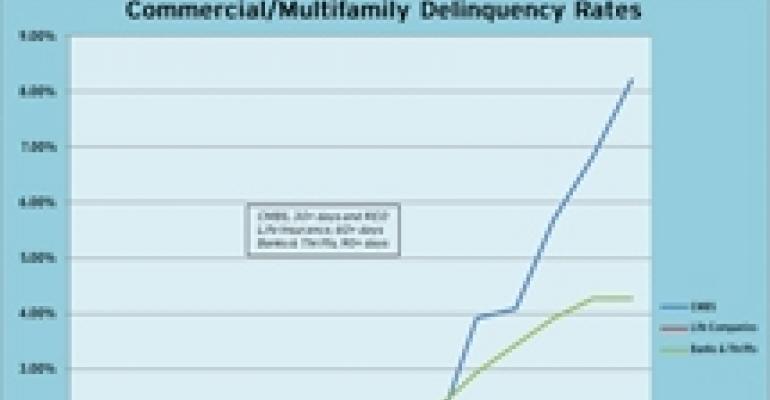

But as the market has turned, CMBS loans have turned sour at an increasingly faster rate than loans originated by commercial banks or life insurance companies. Life insurance companies retained the most stringent lending standards, even during the boom years. They sacrificed market share, but enjoy much healthier loan books as a result of their conservative approach.

The difference in delinquency rates also stems from lenders’ differing abilities to renegotiate with troubled borrowers. Both commercial banks and life insurance companies have more leeway to modify mortgages. Because CMBS loans are securitized, making changes is a more difficult process.

The latest data published by the Mortgage Bankers Association shows that the delinquency rate on CMBS loans now stands at 8.22 percent in contrast to 4.26 percent for loans at commercial banks and just 0.29 percent for life insurance companies. More alarmingly, while the delinquency rate was stable at commercial banks and fell at life insurance companies during the second quarter of 2010, the rate for CMBS loans by 139 basis points.

“Different investor groups lend in different ways and on different types of properties,” Jamie Woodwell, MBA’s vice president of commercial real estate research stated in the MBA’s latest report. “Those differences are becoming more evident as the economy continues to struggle to work its way out of the recession. Life insurance companies, Fannie Mae and Freddie Mac continue to see relatively low delinquency rates on their commercial and multifamily mortgages, the delinquency rate on banks’ commercial and multifamily mortgages appears to have reached a plateau, and the delinquency rate for loans in commercial mortgage-backed securities (CMBS) continued to climb during the period. Performance across all investor groups will continue to depend on economic growth and its ability to generate demand for commercial real estate space.”