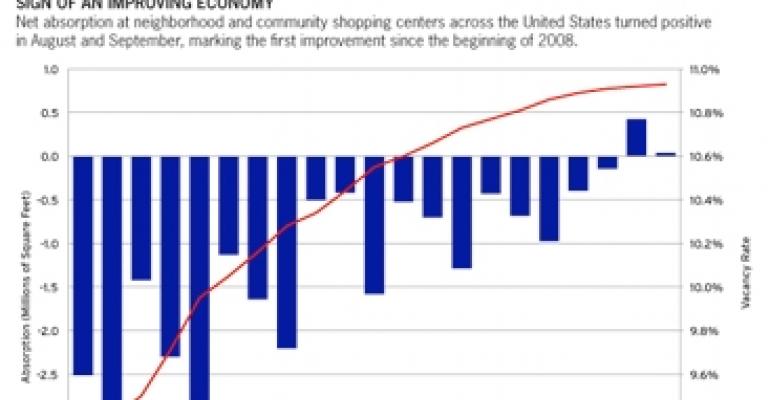

The performance of the retail sector in the third quarter was surprisingly stable. The national vacancy rate for neighborhood and community centers held steady at 10.9%, according to Reis, and about 300,000 sq. ft. of positive net absorption was recorded. This is the first time in over two years that occupied space posted an improvement.

Asking and effective rents nationally remained relatively flat in the third quarter, arresting 10 straight quarters of decline. With higher seasonal activity from retail tenants in the fourth quarter, Reis is projecting a slight rise in rents for the remainder of the year.

Is the worst over?

It is too soon to proclaim that retail fundamentals have bottomed. One quarter’s results do not represent a trend, but parsing the quarter’s results into monthly data shows that there may indeed be room for cautious optimism.

Occupied space declined in July, but net absorption was positive in August and September. Both asking and effective rents posted small increases in August and September, but ended the quarter flat since the rent hikes were not sufficient to overcome the decline in July.

Monthly data tends to be more volatile than quarterly figures, so we may well see negative absorption and rent declines through the rest of the year and through 2011. But at this point it looks like deterioration in retail fundamentals has definitely eased.

Demand drivers

If economic growth has been disappointing and job creation is still in flux, how could retail fundamentals show signs of bottoming? First, although economic growth has been lackluster, the economy has been growing at an annualized rate of about 2.2% since the second half of 2009.

Second, while monthly employment figures may be negative because of government jobs being shed, private sector payrolls have been growing since the beginning of 2010, albeit at a snail’s pace of about 1.2% to 1.5% over the last six months. Firms are posting profits and have been investing in capital and technology, preparing for a ramp-up in aggregate demand.

Recovery in commercial real estate fundamentals typically lags economic growth and job creation by 12 to 18 months. We know the recession ended in June 2009 and that job growth is occurring. So, that means retail fundamentals are likely to bottom out in the fourth quarter of 2010 if they haven’t already.

On the supply side, developers have scaled back significantly. It feels like a lifetime ago, but at the end of 2007 Reis was projecting over 27 million sq. ft. of neighborhood and community center space scheduled to come on line in 2010. This was not an unreasonable assumption since Reis had records of projects planned and proposed for completion that year.

What actually happened? With absorption turning negative in the first quarter of 2008, developers began cancelling and postponing project deadlines. Less than 3 million sq. ft. have come on line through the end of the third quarter of 2010.

We are on track for 2010 to capture the 30-year record for having the lowest number of new completions. Since demand has been tepid, having to put up with less of a supply glut has served as a boon to existing retail properties.

Tempering expectations

Aside from a rise in seasonal activity given the upcoming holiday months, some retailers have been quietly leasing up space as rent levels have been shunted back to levels last seen four to five years ago.

This trend should create some positive momentum for recovery, but any investor who expects retail properties to outperform other types of commercial real estate will be disappointed.

Despite the slowdown in completions over the last 24 months, retail is the one sector in commercial real estate that is relatively overbuilt. With GDP growth and aggregate demand expected to remain in the doldrums, we should expect retail fundamentals to meander, or even show signs of deterioration, through 2011.

In other words, retail fundamentals may have bottomed, but they are likely to continue scraping that trough for some time before gradually posting healthier numbers.

Reis expects the vacancy rate to rise slowly, eventually breaking the all-time high of 11.1% sometime in 2011. That unhealthy level was last observed in the 1990s. We would love to be wrong, but we have yet to record a significant positive change in the economic landscape that would lead us to revise our forecast upward.

Victor Calanog is director of research for New York-based research firm Reis. His column delivers up-to-date analysis and expert opinion regarding property level fundamentals.