There are several metrics that investors can use to identify deals on distressed assets. However, investors typically take a silo approach, focusing on specific property types. Rarely is distress examined across properties. After all, if you’re targeting the office sector, how often do you assess the state of multifamily and retail?

As a first step in zeroing in on specific places where deals might be found, it is useful for investors to evaluate pervasive distress. Does a metro area rank at or near the top of measures of distress across multifamily, retail and office properties?

Despite much talk about market participants looking to deploy capital, transaction activity has yet to pick up. This is partly because of the relative willingness of lenders to adopt workouts instead of foreclosing on distressed assets and selling them at a deep discount.

Two markets that fit the bill

The probability of sellers being willing to reach a deal with interested buyers tends to rise in metro areas where pervasive distress is high. Consider the performance of commercial real estate in Phoenix, Ariz., and San Bernardino/Riverside, Calif.

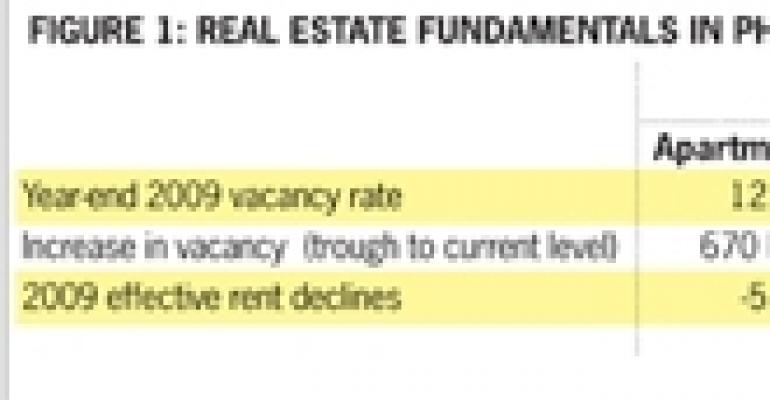

Both markets are experiencing among the highest levels of distress across the multifamily, office and retail sectors. Occupancies have deteriorated so much that vacancy levels have more or less doubled over the last three to four years.

Year-end 2009 vacancy levels are either close to 30-year record highs or worse. Rent declines over the past couple of years have wiped out most of the gains of the last boom, knocking effective rents down to levels observed in 2005 [Figure 1].

Such pervasive distress stands in stark contrast to places like New York City, where some property types have withstood the current downturn better than others. New York office properties have exhibited a lot of distress on the rent side, but multifamily properties held on to vacancy levels at or below 3%, indicating relative tightness.

Not surprisingly, there are plenty of distressed loans supported by properties in Phoenix and San Bernardino/Riverside. As measured by CMBS outstanding loan balances 90 days or more past due across the multifamily, office and retail sectors, these two markets rank among the highest. Both markets are also within the top five MSAs with the highest percentage of properties in foreclosure across all three property types [Figure 2].

A broader look at other categories of distress — including the breakdown of delinquent loans 30 or 60 more days past due and REO properties as a percentage of outstanding balances — reveals similar results. Phoenix and San Bernardino/Riverside rank at or near the top, whether you’re examining multifamily, retail or office properties.

Astute investors must be careful of risks and structural weaknesses that helped cause trouble in the first place. Areas suffering from oversupply of specific property types will continue to see depressed returns in the near term.

Investors will still need to carefully sift through available deals on a market by market basis, but identifying which geographic areas are experiencing pervasive distress offers a useful first step in narrowing their choices.

Victor Calanog is director of research for New York-based research firm Reis Inc. His monthly column delivers insights on performance trends in commercial real estate