Distress is rampant in the retail sector, which leads all property sectors with $32 billion in distressed assets, according to New York-based Real Capital Analytics. But not all retail is created equal. A look inside the numbers reveals that unanchored strip centers, retail in regions plagued by high unemployment and deep housing busts, as well as loans originated in 2006 and 2007, are disproportionately more susceptible to distress.

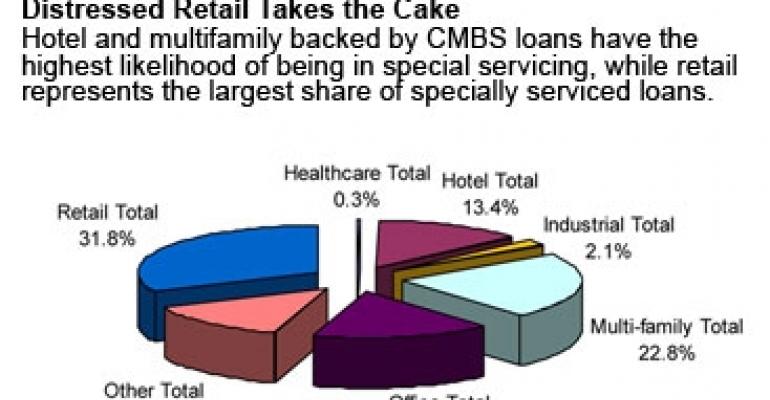

For example, $9.4 billion in retail commercial mortgage-backed securities (CMBS) loans are delinquent, in foreclosure or already taken back by banks, accounting for about 29% of the $32.6 billion of total delinquencies across all property types, according to Horsham, Pa.-based RealPoint LLC.

Markets where the economic crisis has cut sharpest — where housing prices have dropped precipitously and where unemployment is above the national average — have experienced higher levels of delinquencies and distress among retail properties, according to Suzanne Mulvee, real estate strategist with Boston-based Property & Portfolio Research.

Mulvee points to Las Vegas, Atlanta, Phoenix, Orlando and Jacksonville, Fla., as cities where pain is most acute among retail properties. For example, in Las Vegas the unemployment rate hit 13.1% in December and year-over-year home prices were down 26.6%, according to the Standard & Poor's/Case-Shiller Home Price Indices.

In such markets, retail developers attempting to forecast demand for retail may have anticipated tens of thousands of new homes to be built and sold, Mulvee says. When those homes are either halted in construction or completed but left vacant, it creates an obvious problem for retail that was intended to serve those new homeowners. “Banks will tell you that,” she says. “Most of the issues are in their construction portfolios.”

Vintage variation

Another overriding pattern that emerges among distressed retail loans is vintage. Mortgages originated in 2006 and 2007 are more likely to default than retail loans originated in other years. “It’s clear people overpaid for those properties,” says Tom Fink, a senior vice president with Trepp. “The expectations that these properties would generate enough income to pay operating expenses and also cover debt service was wrong. People that bought in 2006 and 2007 got hit by the maelstrom and are suffering now.”

In addition to vintage, property type is another indicator of potential distress. Unanchored strip centers are having greater problems than regional malls, power centers and grocery-anchored strip centers, according to Fink. These properties — typically 75,000 sq. ft. or less — have fallen into trouble quickly by losing just one or two tenants.

For example, smaller centers that had Starbucks as an anchor were hammered by the coffee chain’s decision to shutter hundreds of locations last year. If vacancy falls below predetermined limits, co-tenancy clauses can allow other tenants to exit their lease agreements, potentially turning one or two dark stores into a larger exodus.

One thing that is not affecting the numbers, however, is General Growth’s bankruptcy. Despite the firm’s ongoing restructuring, it has largely remained current on all its debt obligations. Some of its loans are in special serving, but the firm was never delinquent on its payments other than a slight hiccup that delayed payments right around the time it filed for bankruptcy.

Outlook

Most experts think the worst is yet to come for retail and that loans will continue to go bad at a brisk rate throughout 2010.

“Retail is still going to be one of the most troubled assets,” Fink says. “The population has shifted within communities and significant big-box chains have gone out of business with no new concepts to take their place. At one time if OfficeMax closed then maybe Babies “R” Us or Linens ‘n Things or Circuit City would move in. Those retailers are all gone. The space they occupied remains empty, there is nobody to fill it.”

Banks in 2009 added to today’s woes by granting one-year extensions to some borrowers that were having problems meeting their debt obligations at loan maturity. But that process may be near its end. In some cases, banks may have granted extensions in order to allow time to negotiate with borrowers, but after six or eight months with no resolutions it is time to foreclose, Fink says.

Borrowers that were just able to scrape enough money together to make monthly mortgage payments in 2009 also may have trouble in 2010 because of eroding property fundamentals.

“A lot of the banks have been able to extend because the debt service coverage was there, but this is the year where the debt service coverage starts to take the bigger hit,” Mulvee says. That’s because property incomes are continuing to erode as vacancies increase, existing retailers get lease extensions or new retailers sign on at lower rental rates than lenders had projected when the loans were originated.

Inadequate property income may remove the extension option and force more foreclosures, Mulvee says, but that creates a new problem as lenders attempt to liquidate foreclosed assets. Each sold property adds to the data appraisers and investors use to determine market pricing. Foreclosed properties typically sell on the low end of the price spectrum, bringing down overall asset values.

“If they kick too much product they will lower the value of what they are holding,” she says. “They are trying to avoid creating that spiral.”