Properties backed by CMBS loans that have had an appraisal reduction may be a financial fortune cookie for investors. Ordering an updated appraisal is just one of the steps required after a loan has been transferred to special servicing.

In the current environment, most appraisals have been reduced from their original value at securitization, especially loans underwritten during the CMBS boom. “Appraisal reduction is a forward-looking measure of potential future losses,” explains Paul Mancuso, a vice president with commercial real estate data and analytics firm Trepp LLC.

The New York-based researcher recently mined its database to extract all distressed CMBS loans that have had at least one appraisal reduction and still carried an unpaid loan balance through February 2010.

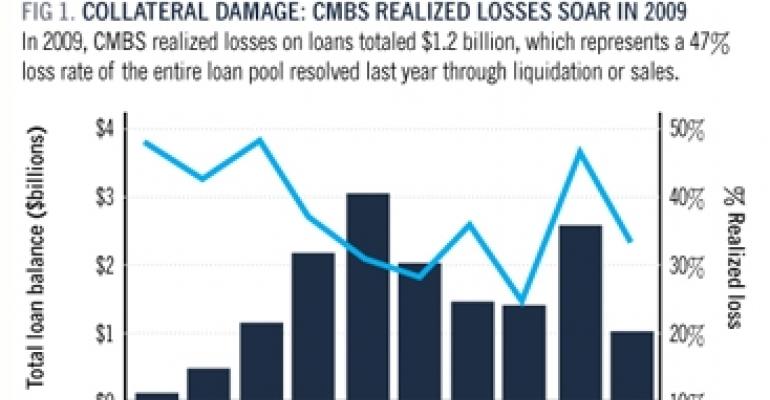

The key metric that Trepp studied is the realized loss rate, or the liquidation balance less net liquidation proceeds received from a troubled loan. The questions Trepp expected to answer: Did commercial real estate values reach a bottom in 2009 when the realized loss rate skyrocketed to 47%? Or is the loss rate of 33% over the first two months of 2010 a momentary blip [Figure 1]?

“Looking at the $33.3 billion universe of loans that have had at least one appraisal reduction through the end of February, our analysis indicates a potential loss rate of just over 40%, or $13.4 billion,” explains Mancuso. “This is 22% higher than the current year-to-date loss rate of 33%.”

Office losses to come

Looking back over time at the universe of loans that realized a loss, there is significant variability in loss rates by property type based on multiple factors, not the least of which is the economy, according to Mancuso.

The lodging sector, negatively affected by the economic slowdown due to a reduction in both leisure and business travel, posted a loss rate of 62.4% in 2009 [Figure 2]. In contrast, the multifamily sector’s loss rate of 63.7% is the result of an overexpansion in heated markets that symbolized the lax lending standards from 2005 through 2007, says Mancuso.

Lodging loans have also sustained the highest overall delinquency rate by property type at 15.65% through the end of February 2010, a record high for the CMBS market, he notes. In comparison, the office sector has had the lowest delinquency rate at 4.33% over the same period.

However, the low delinquency rate for office loans is deceptive. The total dollar volume of CMBS office loans that have had appraisal reductions is $5.1 billion. Of that $5.1 billion total, $2.4 billion has evaporated through appraisal reduction, for a loss rate of 46.1% in the office sector, the highest among the five major property types.

“I don't think we have seen the tip of the iceberg yet for office properties, which continue to struggle with lower rents, tenant concessions and decreased occupancy levels,” he says. “These factors will continue to negatively impact property fundamentals in the near term.”

The greatest realized losses by origination year can be found in the lax underwriting years of 2005, 2006 and 2007 vintage CMBS loans. Across all property types, these years have total realized losses of 44%, 61% and 56.7% respectively.

States of distress

Texas recorded the highest realized loss measured by number of loans and by dollar volume over the June 2001 through February 2010 time frame. At 39.7% [Figure 3], the state’s loss rate is slightly above the 36% portfolio average.

"This was somewhat surprising given the state's large geographic footprint and economic diversity,” says Mancuso. “For example, New York, California and Georgia all had loss rates below the overall average, while Ohio and Michigan, which have struggled for some time now, had loss rates approaching 50%."

The total dollar volume of losses alone — or even losses by loan count — is not the foundation upon which investors should make their decisions. The sheer volume of loans in Texas can be attributed to the massive size of the state, says Mancuso, rather than inherent financial risk such as unemployment or a lack of economic growth.

Mancuso advises investors to look at markets with a potential for future growth, like Georgia, and those markets that have diversified economies that will eventually emerge from the downturn.

Street-level loss

Although unemployment nationally was unchanged in February at 9.7% and some signs of a recovery have appeared in the economy, the pain in commercial real estate is likely to intensify through the end of this year. One disturbing sign of proof: 11 of the top 15 loans by realized loss balance were recorded in the fourth quarter of 2009.

"This is a prime example of basic economic principles. As the number of distressed commercial real estate properties continues to rise, supply will outstrip demand,” says Mancuso. “As a result, a strong possibility exists that loss severity rates will continue to rise in the near term through at least the end of 2010. Due diligence remains key for investors in this environment."