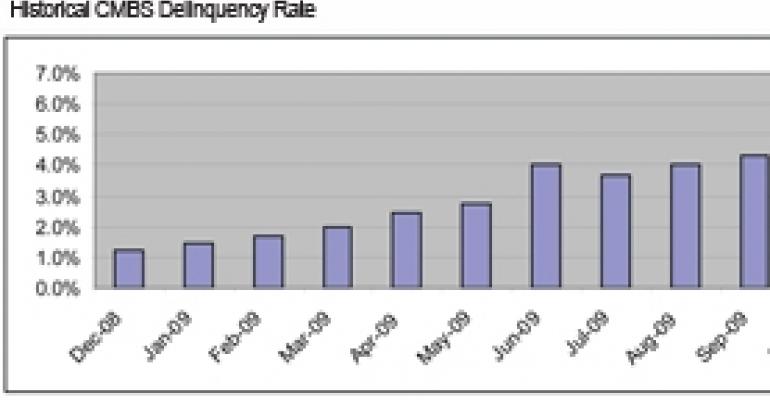

Call it the winter of discontent for the troubled U.S. commercial mortgage-backed securities (CMBS) market. The loan delinquency rate climbed 42 basis points in December to reach 6.07%, making history in the process.

The percentage of loans 30 days or more past due climbed above 6% in December for the first time ever, according to commercial real estate data and analytics firm Trepp LLC.

“It is a scary threshold to have breached,” says Manus Clancy, senior managing director at New York-based Trepp, which tracks some 60,000 CMBS loans totaling $725 billion. “We continue to add 35 to 45 basis points of additional delinquencies per month, so that [trend] really doesn’t seem to be subsiding at all.”

Clancy says that he wouldn’t be surprised if the delinquency rate were to steadily rise to near 8% by mid-2010, but he is quick to point out that Trepp generally doesn’t forecast this type of information.

The hospitality sector continues to be the most troubled performer, although it showed a slight improvement over the prior month. The delinquency rate on CMBS hotel loans registered 13.87% in December compared with 14.07% in November.

The Chapter 11 bankruptcy filing by Extended Stay America in June 2009 accounts for approximately 3.5% of the high delinquency rate among CMBS hotel loans, according to Clancy.

“But you see weakness throughout the hotel sector. It doesn’t matter whether it’s high-end or economy. Everybody is showing lower RevPAR (revenue per available room) and lower occupancies. It’s just not a great story.”

By property type, the multifamily sector posted the second highest delinquency rate in December (9.27%), followed by retail (5.50%), industrial (3.98%), and office (3.42%).

One striking data point is that loan delinquencies for retail rose 72 basis points in December, the largest monthly increase among any major property type.

But the trends in the industrial and multifamily arena were nearly as unsettling with delinquencies rising 65 and 49 basis points, respectively.

While the office sector posted the lowest delinquency rate of any major property type, delinquencies were still up 28 basis points in December.

Possible green shoots

One positive sign is that office rents in some major metros appear to be bottoming out, points out Clancy. “They are not falling as much anymore. That said, they’ve taken some really big hits.”

But there is an even bigger green shoot emerging. While much ink has been devoted to the wave of maturing CMBS loans that many borrowers could find difficult to refinance, three deals completed in the fourth quarter of 2009 are cause for optimism.

In the first commercial mortgage deal sold under the federal government’s Term Asset-Backed Securities Loan Facility (TALF) program, Developers Diversified Realty successfully completed a $400 million bond offering in November.

The risk premium paid to CMBS investors on the triple-A rated class was 140 basis points over swaps. The relatively tight spread served as evidence that investors were willing to jump back into the game on a highly selective basis.

Spreads industry-wide on the super-senior CMBS tranche — the top-rated debt in a bond structure — have narrowed considerably over the past year, according to Trepp.

Spreads on the super senior portion of 10-year CMBS issued from 2005 through 2007 narrowed from 1,200 basis points over Treasuries in February 2009 to below 493 basis points in December 2009.

That was a big victory for the CMBS market, emphasizes Clancy, but uncertainty lingers. “It’s unclear at this point what kind of floor is being placed on those spreads by the TALF program, by the Public-Private Investment Program (PPIP) and so forth,” says Clancy.

“Where would [the spreads] be without the government initiatives? While it’s a bright sign and is evidence that the government programs have had an impact, it’s hard to say where these deals would trade without the underlying support.”

The other two CMBS refinancing deals completed in the fourth quarter of 2009 were not tied to TALF. In mid-December, Coral Gables-based Flagler closed on a $460 million CMBS loan covering its 44 office and industrial properties in Florida.

Banc of America Securities helped Flagler securitize the loan, which was the first non-government supported CMBS issued in 18 months.

Also in December, JP Morgan Chase & Co. sold $500 million of CMBS backed by the Inland Western Real Estate Trust. The deal was reportedly oversubscribed.

According to Reuters, the two top-rated classes in the Inland Western deal sold at yield premiums of 150 basis points to 205 basis points above an interest-rate benchmark, or about one-third of the spread on existing CMBS made at the height of the real estate boom.

While no one is certain how much issuance the U.S. CMBS marketplace will generate in 2010, Clancy is hopeful. “I think it would be great if we got up to $1 billion per month again over the next six months. We started to see these three deals in the late part of 2009. I thought it was a great sign.”