Go to an ICSC event and you'd be hard-pressed to sense there are any deep concerns about the health of the real estate industry.

Booths bustle with activity. Deals are getting done. Developers showcase new activity. And properties continue to trade hands. No one will admit straight out that they are overly concerned about any lingering problems from this summer's credit scare. But beneath the surface, it seems, confidence has fallen off sharply.

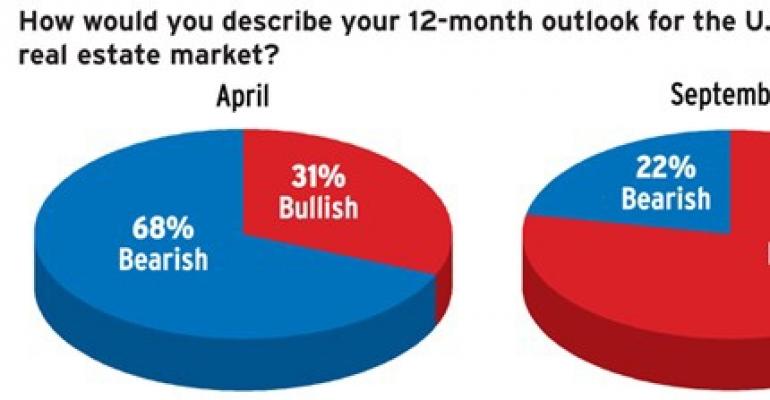

In a survey of 332 commercial real estate industry professionals — conducted by DLA Piper the day after Federal Reserve Chairman Benjamin Bernanke cut the federal funds rate by half a percentage point — a whopping 68 percent of respondents said they were bearish about the industry's prospects over the next 12 months. Asked that same question back in April, only 22 percent of respondents held that position. And the credit crunch is by far the biggest concern for respondents that said they were bearish — a full 66.5 percent pointed to it in contrast with 23.7 percent saying that a sluggish economy and slow job growth were their main concerns.

In another surprise, respondents to the survey don't think the industry's prospects will brighten for another nine months, about 60 percent, in contrast with just 37 percent that thought things would turn around in six months or less.

“I think people see that several factors have to fall back into place,” says Jay Epstien, chair of the U.S. real estate practice at DLA Piper. “They've got to get capital flowing again and bond investors have to buy the paper that's now just sitting at banks. Nobody thinks the capital has disappeared entirely.”

On the debt side, there are also big concerns about the CMBS market. Most respondents, 82.5 percent, anticipate there will be more conventional loans available than CMBS loans during the next 12 months.

Also, 63 percent of respondents admitted they had been involved in transactions delayed or cancelled because of the credit crunch. Still, only a minority, 34.6 percent, though the Fed should take more aggressive action to stabilize the credit markets. Part of that may because a minority of respondents, 26.5 percent, said they had seen an increase in loan defaults.

Not everyone is bearish, though.

John Dowd, senior vice president of development at the Goodman Co., a West Palm Beach, Fla.-based developer that has more than 4 million square feet of projects in its pipeline, thinks any issues in the market will be short-lived.

“The projects that were maybe ill-conceived, were speculative in nature that might have gotten financing a year ago are not going to get financed now,” Dowd says. “But good quality projects with good quality borrowers are still getting a lot of attention from the lending community. That's always the case.”

Dowd says the outlook in the market today is not nearly as it bad in the 1980s or early 1990s when the banking system ground to a halt during the savings and loan crisis. “I think the fact that the rest of the economy is relatively healthy is offsetting some of the concerns about credit and housing,” he says. And, in the end, “growth always cures the problems.”