It can take months, perhaps even a year, to obtain a multifamily loan from the Department of Housing and Urban Development (HUD). Is it worth it? While some borrowers don’t have the patience, more borrowers than ever are saying “yes.”

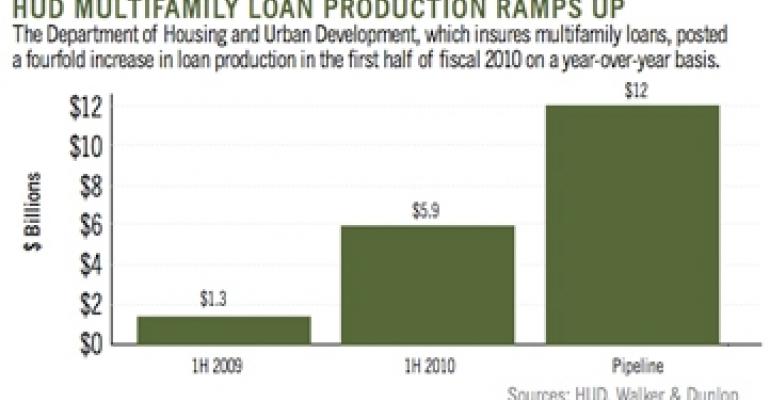

Through the first six months of HUD’s fiscal 2010 — which runs from Sept. 1, 2009 to March 31, 2010 — its multifamily loan program backed $5.9 billion of loans compared to $1.3 billion for the same period in 2009, more than a fourfold increase. HUD lends on skilled nursing facilities, assisted living facilities, hospitals and apartment buildings (age-restricted, market rate and subsidized).

Moreover, fiscal 2009 turned out to be the most prolific year for HUD in its 41-year history. As of March 2010, HUD’s multifamily pipeline was packed with over $12 billion of potential loans.

Indisputable advantages

So, why HUD and why now? First, although HUD has often been referred to as the “lender of last resort,” it may be the only choice for some borrowers. Because of the financial meltdown and the ensuing reluctance by banks to lend money, obtaining a real estate loan from a local or major bank is especially difficult. Many banks cannot afford to provide a loan to a borrower due to the implied risk associated with such a loan. Conversely, HUD is open for business.

Second, it is about simple economics. There are fewer safe places to park money. Because investing in a HUD loan is a safe investment, increased demand by entities that buy a HUD loan equates to lower interest rates for borrowers.

HUD actually is not a lender. Instead, HUD insures a loan. In essence, the buyer of a HUD loan is purchasing an insurance certificate rather than a loan itself. HUD charges a fee for the insurance that ranges from 0.4% to 0.7% of the loan amount, paid annually and is called mortgage insurance premium.

Between HUD and Ginnie Mae (a related party to HUD/FHA), a buyer of a HUD loan is guaranteed that the payment is made on the 15th of each month until the loan is paid off and that the principal is repaid in full. “So what?” you say. Well, the buyer of a HUD loan has a loan that is guaranteed with the full faith and credit of the U.S. government.

Ironic twist

One of the big buyers of HUD loans is that same local bank that did not supply you the loan. The reasoning is simple: If local bank X had supplied the loan directly to the borrower, then local bank X would have had to associate the proper amount of risk with such a loan.

Thus, local bank X’s balance sheet would be negatively affected. Sometimes that risk carries a 50% to 100% risk weighting. The insured loans of Fannie Mae and Freddie Mac, which also are owned by the U.S. government, even carry a 20% risk weighting. A HUD loan carries a zero percent risk weighting.

If, however, local bank X invests in a HUD loan, then the health of local bank X’s balance sheet improves without having to dispose of any of local bank X’s toxic loans. This banking strategy has also driven up the demand and lowered the interest rates for HUD loans.

Diversification of risk

Many HUD loans are pooled together, which gives buyers of HUD loans the benefit of diversification by property type and geography that is often recognized as a lower-risk investment than a single property loan. Since the U.S. government guarantees a HUD loan, the investor is actually analyzing maturity risk as opposed to default risk.

Maturity risk refers to the likelihood of when the borrower will repay the loan. The shorter the time period, the higher the interest rate. A pool of HUD loans will be tranched so that different investors can buy different tranches with each tranche being assigned a different interest rate depending on where in the repayment priority their tranche is.

So what does all this mean? There are more investors investing in HUD loans, which lowers interest rates. Lower interest rates attract more borrowers. With such low interest rates, many borrowers are saying “yes,” the many months it takes to get a HUD loan are worth it.

Douglas W. Bath is group head of the health care finance unit of Bethesda, Md.-based Walker & Dunlop, a real estate finance company. Contact him at [email protected].