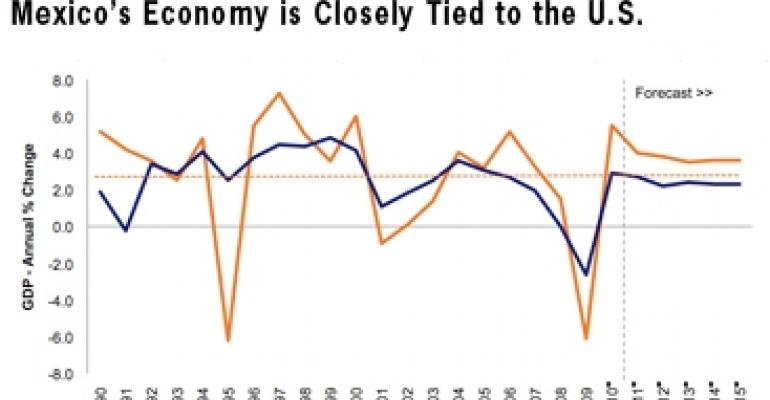

The Mexican economy grew 5.5% in 2010, higher than the general consensus predicted. Following a 6.1% decline in 2009, the 2010 growth rate was the strongest showing since 2000.

During the fourth quarter of 2010, gross domestic product (GDP) grew at an annualized rate of 4.4%, exceeding the pre-recession peak of total output achieved in the second quarter of 2008.

With the United States accounting for 80% of Mexican export sales, growth in the Mexican economy remains closely tied to U.S. performance. Strong GDP growth in the U.S. during the second half of 2010 was largely responsible for Mexico’s surprise performance.

U.S. import demand is expected to remain strong for the next several years, therefore this support will likely filter down to the Mexican economy through a boost in exports and manufacturing output.

The Economist Intelligence Unit (EIU) forecasts Mexico’s GDP growth rate to expand at an average annual rate of 3.7% from 2011 through 2015, higher than the 3.1% average achieved during the period 2003 through 2008, and 230 basis points higher than the average over the past 20 years. This higher growth rate reflects the stronger long-term prospects in Mexico.

Following a monthly increase in the Consumer Price Index in Mexico during the second half of 2010, the inflation rate slowed in the beginning of 2011. As of April 2011, the inflation rate was 3.4%, 70 basis points below the 2010 average.

Given the Mexican central bank’s (Banco de México) target interest rate of 4.5%, the decline gives some respite to the central bank’s inflation targeting priorities.

The moderate inflation rate is important at a time of rising global commodity prices, and should provide the ability to delay increasing interest rates at an early stage of a recovery period, according to the EIU.

The EIU forecasts Mexico will experience a GDP growth rate of 4% and an inflation rate of 3.5% in 2011, and a similar trend of strong growth with moderate inflation through 2015.

This combination is attractive to investors, especially when compared with other Latin America countries, such as Brazil, that are contending with higher inflation rates and currency values.

According to ING Financial Markets Research, Mexico’s currency remains the cheapest of the 18 global emerging markets tracked in the ING Purchasing Power Parity survey.

The value of the Mexican peso remains well below the highs experienced prior to the financial crisis of 2008 and 2009. Investors demand a greater compensation for the uncertainty of inflation or currency values, and Mexico is not currently experiencing either of these trends.

Mexico’s access to the U.S. market, integration into U.S. manufacturing supply chains, extensive network of free-trade agreements, and a large internal market make it one of the more attractive investment locations among emerging-market economies.

As a result, Mexico is the third largest trading partner in the U.S., behind only China and Canada.

After losing significant market share to China during most of the 2000s, Mexico captured a larger portion of the total trade balance of the United States in 2010.

This marked the first time since China entered the World Trade Organization in 2001 that Mexico posted a larger gain of the U.S. market share than China. Mexico maintained its U.S. import market share during January and February of 2011.

Two primary factors are contributing to Mexico’s attractiveness: high energy costs and costlier Chinese labor. High energy costs make Mexico’s close proximity to the United States more advantageous than shipping goods across the Pacific Ocean.

Mexican labor is estimated to cost 14% more than Chinese labor, a drastic change from the 240% difference recorded in 2002, according to Reuters. If these trends continue, both present Mexico with the opportunity to further increase its share of the U.S. import market.

Increased violence in Mexico, particularly during 2010, has eroded some of the gains the country made in terms of perceived investment risk and political stability.

Consequently, tourism and investment in particular areas of the country will continue to be negatively affected, while recent police reforms will require time to take effect.

Real estate outlook

The improving economic fundamentals during 2011 have spilled over to the real estate industry. The industrial real estate fundamentals are improving, driven by strong manufacturing growth associated with U.S. demand.

Additionally, while retail spending struggled through the downturn and has recovered only modestly to date, higher disposable incomes and private consumption are expected to support the retail sector in the medium and longer term.

In March 2011, Mexico launched its first real estate investment trust (REIT), or FIBRAS as they are known in Mexico, to be listed on the Mexican stock exchange. According to The Wall Street Journal, the initial public offering raised US$300 million (MX peso $3.62 billion) by selling 185.4 million certificates at US$1.61 each.

“Fibra Uno” will use proceeds from the global offering to acquire three properties and consolidate an existing portfolio. The existing portfolio includes 13 properties, composed of industrial, retail, office, and mixed-use assets. The other three properties will be acquired post closing.

The initial idea for FIBRAS listings in Mexico was proposed in the early 2000s. However, tax and regulatory issues needed to be established prior to launching the first one. REITs provide enhanced liquidity to the real estate market and should serve this function in Mexico, if and when the structure is more widely utilized.

While REITs may add greater liquidity to the sales market, we expect further strengthening of real estate fundamentals to also enhance investor appetite. The limited construction and positive absorption should further lower vacancy rates and stabilize or slightly grow rents, especially in the second half of 2011 as the economic recovery takes hold.

Sustained growth rates over the next couple years should help real estate markets recover to pre-recessionary levels. In the long term, the large, young and growing population in Mexico and its strategic location relative to the United States create a strong investment rationale with attractive risk-adjusted returns.

David Lynn is a managing director, generalist portfolio manager and head of investment strategy for ING Clarion Partners in New York.