Several major pension funds have announced cutbacks in their investment in the stocks of publicly traded real estate investment trusts, even though REIT stocks outperformed many market indices in 2010.

The nation’s largest public pension fund, the California Public Employees’ Retirement System (CalPERS), announced in February it is phasing out its investments in REIT stocks as part of its real estate portfolio over the next three years. Currently, REITs make up about 7% of the CalPERS real estate portfolio.

According to a statement from the National Association of Real Estate Investment Trusts (NAREIT), an industry trade group, “The real estate staff’s recommendation to the CalPERS board is inappropriate and ill-advised.”

That sentiment was echoed by one of CalPERS’ own consultants, Wilshire Consulting. The firm questioned the strategy, arguing that having REITs as part of the property portfolio enabled the pension fund to be nimble in regulating its real estate exposure.

Still, other pension funds have adopted similar strategies to CalPERS. The Nebraska Investment Council, with a real estate portfolio valued at $416 million, plans to withdraw its entire $44 million investment in REITs by the end of 2011.

The council’s first real estate investment was in REIT stocks in 1994, but the times have changed. “Volatility in the REIT space is an issue for the pension fund.” says Jeff States, investment officer for the Nebraska fund.

Real estate management advisor The Townsend Group recently recommended that the San Diego City Employees Retirement System reduce its allocation to REIT stocks from $116 million, or 27% of its real estate assets in 2010, to around $80 million, or 20% of its real estate assets in 2012.

The $23 billion South Carolina Retirement System, which hopes to finalize its first real estate investment strategy by mid-2011, has decided not to invest in REIT stocks. Its real estate consultant, NEPC, recommended the move, citing concerns about REIT stocks’ correlation to small cap stocks.

That notion is a relatively recent development, since only a few short years ago REITs were considered a contrarian play. But along with their popularity and stellar performance, they are now considered more in step with the broader stock market.

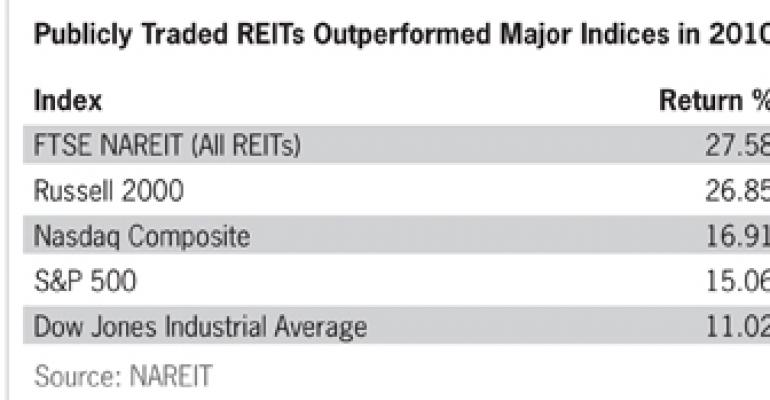

The recent pension fund moves come as a dramatic turnaround as well. Over the past few years, pension funds have been buoyed by the performance of REIT stocks. In fact, in 2010, REITs gained nearly 28% on a total return basis, easily beating the S&P 500 return of 15%, according to NAREIT (see chart).

In February, NAREIT released a new report, the Real Estate Optimizer, directed to pension funds extolling the virtues of combining one-third part REIT stocks with two-thirds real property in their portfolios to produce optimal returns.

But apparently their recent success comes with a price, as many analysts question their potential growth trajectory in the months ahead.

“Many of the REIT stocks demonstrate a strong correlation with overall market returns,” says Sam Chandan, global economist for New York-based researcher Real Capital Analytics. “A larger REIT position introduces an exposure to the stock market that won’t be appropriate for every pension fund.”

An October 2010 study by the Pension Real Estate Association (PREA) found that since 1994, returns for REIT stocks beat private equity fund returns by 1% per quarter, but were found to be three times more volatile. When adjusted for risk, private equity funds outperformed REITs over the same period.

PREA research director Greg MacKinnon notes that ultimately it is not a case of having REITs or not having REITs. Given the study’s findings, there is room for both REIT stocks and private equity funds in a balanced portfolio, but that balance is dependent on the risk profile of the particular fund.