It’s been a long time coming, but investment sales specialists say deal activity in the retail sector may be poised to surge.

The market for retail properties has shown clear improvement throughout 2010. In the first eight months of 2010, investment in retail properties amounted to $22 billion, according to CoStar Group figures. In contrast, the full year figure for 2009 was $12 billion. “It’s still not what investors would like to see, but it’s definitely improving,” says Suzanne Mulvee, senior real estate economist with the CoStar Group, a Bethesda, Md.-based research firm.

But there are signs that deal volume may jump by an even greater degree through the end of 2010 and into 2011. Firstly, after waiting for more than a year to start dealing with the distressed assets on their books, lenders are feeling healthy enough to begin disposing of some of their troubled real estate, industry sources say. Moreover, institutional and private investors that have amassed war chests are ready to pounce on the deals that may come to light.

In fact, anecdotally sales brokers say they are seeing a clear rise in activity. For example, in August, Tom J. Lagos, senior vice president and director of retail services for the Greater Los Angeles area with Colliers International, sold six retail properties. In contrast, in August 2009 he closed only two deals. He attributes the increase to greater financing availability and a more optimistic outlook on leasing activity in the retail sector, as well as attractive pricing. Lagos specializes in selling better-positioned, multi-tenant shopping centers valued at $10 million or greater.

In addition, several large portfolios might soon change hands, notes Dan Fasulo, managing director with Real Capital Analytics, a New York City-based research firm. Portfolio deals serve as a sign of health because they show that buyers are finally able to secure the large loans necessary to complete portfolio acquisitions. In 2008, the low point in this cycle, almost no portfolios traded hands. Fasulo expects retail sales activity to accelerate throughout the fall.

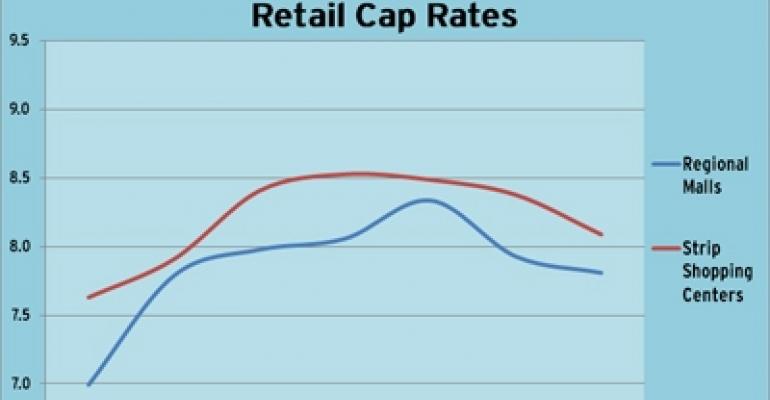

To date, much of the activity that has been occurring has centered on class-A properties in core markets. As a result of transaction activity being skewed toward best quality assets, cap rates in the retail sector have showed improvement in recent months, according to the Korpacz Real Estate Investor Survey for the third quarter of 2010, produced by PricewaterhouseCoopers.

The survey, which is based on the opinions of a cross section of institutional investors, found that the average cap rate for regional malls declined 12 basis points from the second to the third quarter of 2010, to 7.81 percent. The average cap rate for strip centers declined 29 basis points, to 8.09 percent, and the average cap rate for power centers declined 32 basis points, to 8.38 percent.

However, experts are predicting that in the coming months more distressed properties will enter the fray, as banks begin to dispose of the worst parts of their real estate portfolios, says Gerard Mason, executive managing director in the New York City office of Savills LLC, a real estate services provider. Both Mason and Mulvee warn that the long-predicted tsunami of distress will likely never materialize, but there will be a continuous trickle of distress assets being put on the market as banks’ profits improve and they find themselves able to absorb the losses.

“There is increased sales activity and you can see it all over,” Mason says. “If you talk to acquisition people at funds they are seeing an increase in the number of offerings. We are doing two or three times the number of opinions of value that we were doing last year, in preparation for sales. We are seeing more beauty contests, more potential sales being teed up for the first quarter of next year. And we are seeing it on all product types, particularly retail.”

Investors interviewed for the Korpacz survey predict that over the next six months cap rates on retail transactions will either remain at their current level or compress further. But Mason expects that as more class-B and class-C product begins to trade, average cap rates might inch higher, perhaps by 100 to 150 basis points. The increase would spur on further acquisition activity by providing opportunities for investors interested in distressed and value-add assets.

“I think you are going to see lesser product coming out in more abundance and prices will come down across the board because the quality will even out,” Mason says. “And that’s the way it used to be—there was something for everybody out there.”