With investment sales volumes nearly at a halt, investors have continued to hoard capital as they wait for prices to fall further. Yet in the current climate, where those with access to capital remain in the driver's seat, questions linger as to how much liquidity exists and what properties are actually worth. As a result, there remains great uncertainty as to when money will start to move back into the retail real estate market.

"Is there cash on the sidelines? Absolutely. Both in pension funds and institutions, as well as private wealth," says Anthony F. Buono, executive managing director of retail services for the Americas at CB Richard Ellis. "There has probably never been a time when there has been that much capital set aside in short-term instruments due to the volatility in the market."

As of January, $8.85 trillion was being held in cash, bank deposits and money-market funds, according to Federal Reserve data compiled by the Leuthold Group, a Minneapolis research firm, and Bloomberg. That volume is nearly equal to the current market capitalization of the entire U.S. stock market. Money market holdings alone hold a historic high of $3.86 trillion as of March 25, according to data from the Investment Company Institute, an association of investment companies based in Washington, D.C.

"Anecdotally, we're getting calls frequently from money managers and hedge funds suggesting they are sitting on hundreds of millions of dollars in capital, and there also is a wide range of investors in the $5 million to $75 million liquid market that allege to have capital," says Bernard Haddigan, managing director of the national retail group at Marcus & Millichap in Atlanta. Those investors are all looking for the same thing – bargains, and those value-priced properties have been slow to emerge, Haddigan adds.

Investors such as AEW Capital are flush with cash and in no hurry to spend a dime. The Boston-based pension fund advisor is sitting on about $2 billion in capital from clients throughout North America. Like many investors, AEW is waiting for more attractive cap rates. "This is a market where you don't have to rush. We're not trying to force any deals in this marketplace," says Mike Acton, director of research at AEW Capital. AEW Capital purchased about $226 million in retail properties in 2008, and the firm has not set a firm target goal for 2009 acquisitions.

Some REITs have also bolstered their balance sheets for potential deals. For example, Indianapolis-based Simon Property Group currently has priced an equity offering of 20 million shares and 3 million shares to cover overallotments at $50 per share, which will net the firm $1 billion to $1.2 billion in cash. The firm ended the quarter with $1.1 billion in cash on hand and access to more than $3 billion under its revolving credit facility. It also has dealt with much of its upcoming expiring debt. As a result, Simon has incredible buying power to tap.

Waiting for a price shift

However, this cash is being amassed at a time when the broader commercial real estate market is recording its lowest level of sales activity since the early 1990s. Sales of retail properties have slowed to a trickle, with 128 properties valued at $1.8 billion trading hands during the first quarter of 2009. That volume is less than one-quarter of the 592 properties valued at $7.1 billion that sold during the same period in 2008, according to New York-based Real Capital Analytics. In 2007, the first quarter volume amounted to 991 properties for $18.8 billion. The research firm tracks real estate sales valued above $5 million.

The lack of deal flow can be blamed on several factors–the continuing gap between bid and ask prices, uncertainties in the market, and the ongoing crisis in financial markets. All of those hurdles are contributing to investors' decisions to keep capital on the sidelines. The biggest stumbling block for many is the perception that prices remain high. Cap rates on completed retail deals were 7.32 percent during the first quarter, according to Real Capital Analytics. That's less than 100 basis points above the low of 6.56 percent recorded in the second quarter of 2007. However, most observers in the market think that retail property values are down at least 25 percent from peaks and may fall 40 percent before all is said and done.

As a result, the gap between bid and ask prices remains sizable. In some cases, the difference between the bid and ask spread is as high as 20 percent to 40 percent, says Dan Fasulo, managing director at Real Capital Analytics. "In that type of environment where sellers and buyers can't agree on pricing, it's pretty easy to see why sales activity would come to a screeching halt," he says.

So how do you resolve this disconnect between the data, bid/ask gap and broader perception that values need to fall further? For one, Real Capital's figures only cover completed deals and for the most part the properties changing hands are higher quality. So that's skewing the figures some. The cap rate on offered deals (as opposed to closed), for example, was 7.68 percent. In the past, Real Capital had recorded offered cap rates lower than closed cap rates. Some brokers think that if more lower quality and distressed assets were trading today, cap rates would be at least 200 basis points above the 2007 low. As a result, some properties will eventually trade for cap rates higher than 9 percent or 10 percent.

Yet most sellers remain stubborn on prices. Where they can, owners are opting to wait out the market--particularly if they have a property with good cash flow. That means the most likely assets to hit the market in coming months will be situations of distress where either a property is hurting or where an owner is coming up against a refinancing deadline and can't arrange a new line of credit.

"The reason that people have these expectations of steep discounts is because there is virtually no debt available," Haddigan says. Private capital can only afford so much in terms of what they're buying. Investors also have increased yield requirements due to market uncertainty and the belief that the U.S. is in a prolonged economic downturn. "Some investors have yield requirements of 25 percent to 30 percent on an annualized basis if they are going to be taking risky positions," Haddigan says. Most sellers can't–or won't–drop prices that low.

Another reason buyers are taking their time is that they have a variety of alternative investments to choose from right now. Discounted properties are emerging in all commercial property types. At the same time, other options such as distressed debt and REIT stocks are trading at incredibly low levels, and for those buyers willing to take on the risk, they could produce big returns. That being said, investors are continuing to shop for viable retail real estate buys whether their strategy is to buy and flip or take a long-term hold position.

Distressed sales ahead?

Many buyers are biding their time, hoping to pounce on real estate bargains. Distressed retail properties have already started to hit the market, and many anticipate that a surge of distressed retail properties will emerge later this year. "So no one wants to pay retail price for a property when they can buy in a couple of months at the wholesale price," Fasulo says.

In fact, some industry observers believe that distressed property sales will serve as a much-needed catalyst to revive the floundering commercial real estate investment market. "What will emerge in leading us out into more sales activity will be private equity. They will see distress as an opportunity, and they will be the first movers to take risk," Buono says.

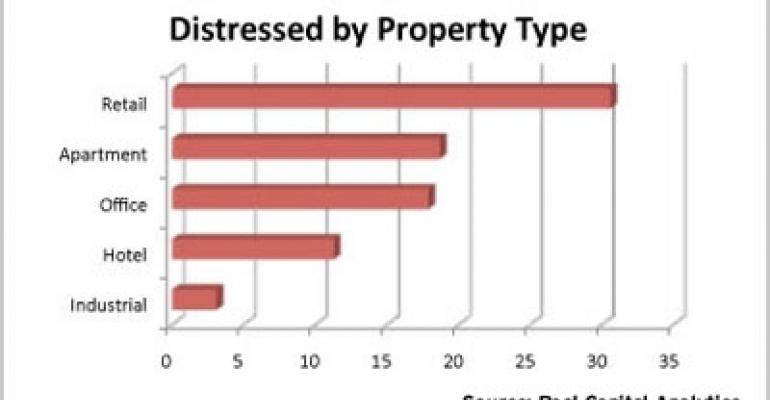

The volume of distressed retail properties is on the rise. Since September, about 3 percent of all retail sales have been associated with a distressed situation, largely sales from former lenders that have foreclosed on assets. The current volume of distressed retail assets on the market at the end of April reached 1,276 properties valued at $30.6 billion, according to Real Capital Analytics. That makes it the property type with the greatest volume of distress. Overall, Real Capital estimates the value of distressed properties across all commercial real estate property types to be $81.6 billion.

There has been a trickle of distressed properties that have hit the market over the past 60 days with attractive prices that are below replacement cost. "That being said, there are still a number of sellers, including banks, that are doing their best to hold onto assets and not put them on the market at a big discount," Fasulo says.

The volume of distressed retail assets that may eventually land on the for-sale market is uncertain. Some industry observers believe there will be a "flood" of distressed properties for sale in late 2009 and into 2010 as the shake-out among retailers continues, and owners battle against falling cash-flows and refinancing challenges.

Others believe that the supply of discounted properties will be more modest. Owners may find more success hanging onto their properties, and some distressed properties that hit the market may not be desirable at any price. Many lenders, for example, have shown a willingness to grant forbearance to put off foreclosures, taking an "extend and pretend" mentality. Banks, dealing with mountains of other sorts of bad debt, are loath to take on ownership of commercial real estate in the current climate.

"We have definitely been out looking for deals for the last four to five months in the mid-south, and those deals are proving to be scarce," says Allen McDonald, a principal at Baker Storey McDonald Properties, a Nashville-based real estate investment firm with a 650,000-square-foot portfolio of retail properties. BSM's goal is to acquire $100 million in assets over the next 12 to 18 months. Whether or not the firm will be able to find enough properties that match its investment criteria remains to be seen.

BSM is currently negotiating for the purchase of a $10 million community retail center in the southern U.S. "What is motivating us to move on this particular asset is that we feel like we are getting it at a good discount to replacement cost," McDonald says. Because the property has a motivated seller, BSM is negotiating a price that is 40 percent to 45 percent of replacement cost. The property also has good tenancy and a good infill location, he adds. Finding – and closing – on such deals is not easy. Firms have to be nimble and adept at underwriting, because the market remains very competitive, he adds.

Timing the market

The big question for many is when the stand-off between buyers and sellers will end, and investors will start moving capital back into retail real estate acquisitions. "I wouldn't be optimistic that there will be a flurry of transaction activity this year," Buono says. Although there are sellers today that are getting closer to that price gap, Buono anticipates that it will likely be 2010 before sales activity picks up.

Because lenders are working hard to avoid loan foreclosures, by extending terms and offering flexibility on payments, it may be late summer or fall before the dam breaks on troubled retail properties, Haddigan says. However, lenders are going to be forced at a certain point, because of the amount of distress, to start filing notices of defaults and mark-to-market their assets to be taken over by the FDIC.

"Eventually, we are going to see an acceleration of distressed properties on the market, and the three worst segments are going to be retail, hospitality and office," Haddigan says. However, Haddigan admits that it could be mid to late 2010 before the real estate investment market is in the "eye of the storm" for distressed sales. "People don't want to catch a falling knife," he adds. "People don't want to buy now when prices are likely to continue to fall."