Green shoots of spring are finally appearing as warm weather fronts begin to make a welcome return to the U.S. Denver recently notched 81 degrees, Chicago reached into the 70s and even Boston got above freezing, recording a balmy 55 degrees. Weather in the U.S. is clearly in transition as we move from winter to spring. While this transition brings welcome relief from frigid temperatures, spring also brings stormy weather. Similarly, the financial environment will become increasingly unstable as central bank policies across the globe move in different directions. Just as opposing weather fronts create instability, opposing central bank policies will inevitably create heightened instability in the financial markets. And this is even before taking into account the opposing views of the market and the Federal Reserve as it relates to interest rates.

Opposing monetary fronts hit home

The U.S. economy is slowly transitioning off of monetary life support. More than 3.1 million jobs were created in 2014—30 percent more than in 2013, 24 percent more than during the best year of the previous economic expansion, and the most since 1999. Assuming the March jobs report was an aberration, speculation is increasingly focusing on when the Federal Reserve will take the next step in raising short-term rates. Conversely, due to weakening economies, the European Central Bank (ECB), Bank of Japan (BOJ) and People’s Bank of China (PBOC) are all ramping up easier monetary policies in hopes of stimulating their cooling economies.

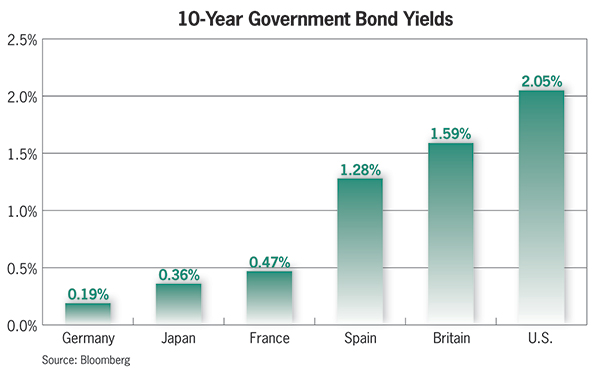

ECB policy has helped push German 10-year bond yields down to 0.20 percent from 1.57 percent at the same time last year—a massive decline. More importantly, this means that U.S. 10-year Treasuries are now more than 180 basis points higher than equivalent German Bunds.

Meanwhile, the BOJ has also had success in exerting downward pressure on Japanese interest rates, where 10-year Japanese government bonds now stand at 0.36 percent, down from 0.62 percent at this time last year. Not to be outdone, the PBOC is also engineering its interest rates lower, with 10-year debt declining to 3.56 percent from 4.48 percent at this time last year.

The U.S. economy and Fed policy are moving in opposite directions of the European, Japanese and Chinese economies, as well as their respective central banks’ policies. While these events are thousands of miles away, there are implications for domestic commercial real estate investors that will reach into underwriting assumptions, investment committee deliberations and investment strategies.

First, these opposing policies will likely cause heightened instability in the financial markets. The rapid ascent of the dollar can become problematic for global financial stability as continued declines in foreign currencies, if unabated, may lead to currency crises, especially in markets highly dependent on foreign domestic investment and/or those that have been borrowing in U.S. dollars. Even absent a destabilizing currency crisis or other financial instability event, increasing financial market volatility will drive investors to U.S. Treasuries in spite of Fed actions, placing downward pressure on long-term interest rates. This can impact real estate underwriting assumptions, including the cost of capital and terminal cap rates and, as a result, going-in cap rates and pricing.

Second, setting aside increasing financial market volatility, the actions of foreign central banks are already having an impact on U.S. real estate. While everyone is hyper-focused on when the Fed will raise short-term interest rates, commercial real estate investors in this country would be wise to keep at least as much of a focus on foreign central bank policies. Just as we seek out the best real estate investment opportunities across the markets we invest in, sovereign debt investors look for the best opportunities across the countries they invest in. Due to foreign central bank policies, U.S. Treasuries look very attractive when compared to a variety of sovereign debt alternatives, especially when considering that foreign currencies are depreciating in relation to the U.S. dollar.

This serves to put downward pressure on long-term U.S. interest rates, impacting both underwriting assumptions and demand for commercial real estate for investors.

Third, some financial market volatility can be beneficial to commercial real estate pricing. Investors correctly view commercial real estate as a safe port in the storm. For example, commercial real estate returns have been positive 32 out of the past 36 years or 90 percent of the time.

Commercial real estate’s income returns are even more impressive, posting a perfect record of positive income returns 36 out of 36 years, all while averaging 7.5 percent.

As financial markets become increasingly volatile, commercial real estate’s relatively stable return history and consistent source of income should become increasingly valued by investors providing future price support for the asset class.

Investment implications

Given expectations of stormy financial market conditions, should investors take cover and batten down the hatches? We are not recommending heading to the storm-cellars. Rather, grab your wind-resistant umbrella and avoid exposed areas.

Assets with longer-term leases should provide an umbrella of stable income to shield your core portfolio against the inevitable inclement weather it will face over the next few years. If you are going to go out without an umbrella, do it sooner rather than later, taking near-term lease-up risk as opposed to later lease-up risk. Lastly, whether you choose the protection of stable income or venture out on being less protected, avoid exposed areas—namely, markets with an excess of open space that can quickly turn into competing supply. These markets should also be avoided at this point in the cycle because they take longer to recover after a downturn. Following these steps will help prepare you for the increasingly volatile environment that we will all be facing in the near-term.