The impact of lower oil prices on the U.S. commercial real estate market can be analyzed from two perspectives: the direct impact and the indirect impact.

The indirect impact of lower oil prices

The impact of lower oil prices on commercial real estate markets has largely been indirect thus far. That is, lower oil prices have hurt the global economy due to the dependency of a number of countries (Venezuela, Norway and most of the Middle East) on oil exports. The depressed demand in these countries has triggered a multiplier effect across the world and has fueled fears of deflation. In the U.S., this has lowered demand for U.S. exports and has hurt stock prices.

Few are able to measure the overall impact from lower oil prices on U.S. economic growth or determine when oil prices will turn around. Thus, not only has the uncertainty from the global outlook lowered expectations for growth across the U.S. economy, but uncertainty on the uncertainty tends to cause stock prices to gyrate wildly. This lack of clarity—that the media feeds on a daily basis—may affect the decision-making process for landlords and tenants, as well as developers, investors and lending officers who may stall on buying, selling, leasing, investing in or building properties.

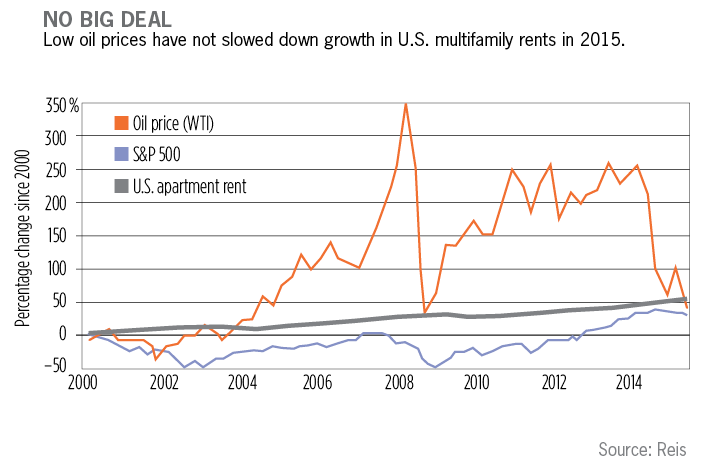

Still, despite the doom and gloom reported in the media, the impact from lower oil prices has yet to be seen in overall real estate statistics. Apartment asking rents in the U.S. climbed 4.6 percent in 2015, slightly above what we had forecasted as of the third quarter for year-end growth, which was 4.5 percent. Office rents climbed 3.1 percent in 2015, which was slightly lower than our third quarter forecast of 3.3 percent. The annual (2015) rent growth for retail and industrial properties was also only 10 and 20 basis points lower, respectively, than we had forecasted as of the third quarter.

Also note that other global risk factors include slower growth in China that has affected growth in other countries such as Brazil and those dependent on commodity exports. While it is nearly impossible to measure the separate impacts from lower oil prices and problems in China, it is safe to say that both are affecting stock market volatility, as well as economic expectations.

But we should be clear that growth in commercial real estate statistics has been driven by steady job growth, the leading determinant for real estate demand. The outlook for both GDP and job growth remains positive as is our outlook for real estate statistics.

That being said, we have revised our forecasts somewhat to recognize a lower overall growth rate across all property markets going forward, yet we still show positive growth for each in all years.

The direct impact of lower oil prices

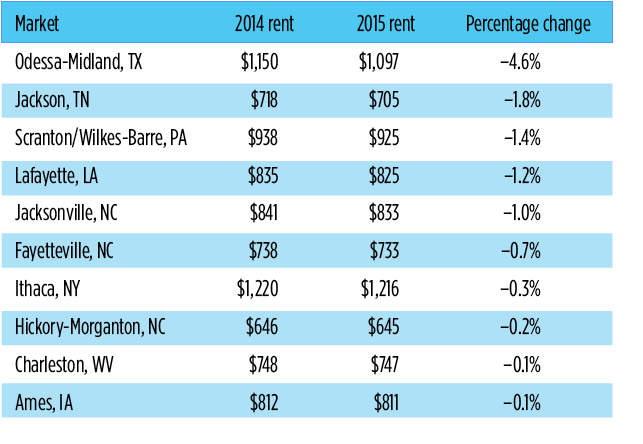

A number of markets across the U.S. have grown tremendously over the last few years due to the growth in shale and other oil drilling. Most of the metros that have seen strong growth from oil and drilling are tertiary markets according to our classification system. In fact, a look at the annual apartment rent growth rates for 2015 shows that only 10 of 275 markets had a decline in rent growth, and all of them were tertiary markets. These markets are listed in the table below. Note that only Odessa-Midland saw a significant decline in rent.

Even markets such as Houston saw apartment market rent growth of 4.6 percent in 2015. Dallas’ rents grew by 4.8 percent, Fort Worth’s by 3.7 percent, Austin’s by 5.1 percent, San Antonio’s by 3.8 percent. Denver, which relies on the oil industry to some degree, grew by 6.8 percent, the sixth highest rate of the 275 markets. Boulder was fifth at 6.9 percent.

As for the office market rent growth, all of the previously mentioned markets had positive growth in 2015, and both Dallas (+4.1 percent) and Austin (+3.4 percent) posted growth rates above the U.S. average (+3.1 percent). Houston office rents grew by 2.3 percent, Denver’s by 2.8 percent. Many of these cities were more deeply affected in earlier oil busts, but they have since diversified their economies and thus have shielded themselves from oil shocks such as the most recent one.

In sum, any further volatility in oil prices will continue to affect stock market prices and potentially the real estate market, but largely in a macroeconomic and indirect way by creating uncertainty on the decision making of market participants. As long as job growth remains positive, the real estate market will remain positive as well. Some smaller areas that have shed jobs from drilling and ancillary oil demand will continue to decline, but these markets are isolated and generally small.

The chart below illustrates the clear difference between the stability of average apartment rent growth versus the volatility in oil prices and the S&P 500.