Up until recently, lenders and special servicers have done little to deal with the mounting volume of distressed mortgages in CMBS pools because it is so difficult to get all interested parties on the same page. But now the sheer volume of distress is forcing their hand.

In March, the unpaid balance on CMBS loans transferred to special servicing reached a trailing 12-month high of $79.83 billion, of which retail loans accounted for about 25 percent of that total, according to Realpoint LLC, a Horsham, Pa.-based credit rating agency.

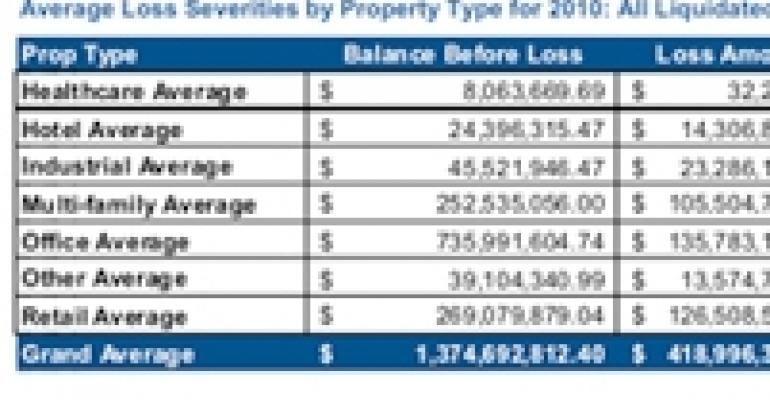

Overall, special servicers remain reluctant to liquidate distressed loans because that would mean selling foreclosed properties at a loss. So far this year, the loss severity on liquidated retail loans has averaged 47.9 percent, according to Realpoint.

In an effort to keep loans alive for as long as possible, servicers have tried all sorts of tactics. For example, loan extensions remain a popular strategy. In cases where CMBS-financed mortgages on cash-producing retail properties come to term earlier than other mortgages in the same CMBS pool, servicers are often extending the mortgages to match the deadlines of the entire pool, says James DuMars, senior vice president and managing director in the Phoenix office of NorthMarq Capital, a real estate investment banking firm.

Even if the term of the mortgage and the term of the pool mature at the same time, special servicers in some cases are still willing to grant extensions of up to three years. But those extensions might involve so-called cash flow sweeps with the lender collecting any income after a property’s operating expenses and other fees have been paid, DuMars notes.

“Every tranche in that securitization is happy with that solution,” says Gerard Mason, executive managing director in the New York City office of Savills LLC, a real estate services provider. It’s a different picture than six months ago, Mason explains.

At that time, holders of subordinated debt faced the prospect of being wiped out completely. Meanwhile, holders of the top-rated tranches were unhappy until about six months ago because they wanted to foreclose and get 100 cents on the dollar.

Now that AAA bonds have risen back to par value, senior holders can sell their bonds on the secondary market to recoup their costs. And holders of the riskiest bits are doing better as well because the restructuring provides for interest payments to be kept current.

Tough choices for servicers

Loans on retail properties that are distressed because of falling net operating income tend to be trickier to resolve because they require modifications that involve taking losses, experts say. Whenever possible, special servicers prefer to keep existing borrowers in place, rather than liquidate loans or transfer them to new owners.

But to modify CMBS loans, servicers typically need borrowers to put up additional capital, says DuMars. Even if a borrower has an excellent reputation and a proven track record in operating retail assets, a servicer has a hard time justifying a workout to the note holders.

In addition, if the center in question has vacancy issues, a borrower who can’t come up with additional cash likely won’t have the necessary funds for tenant improvement allowances and other perks necessary to attract new tenants.

“The servicer can find a lot of good property managers,” DuMars says. “People have to realize the servicer is going to do what’s best for the trust.”

If the borrower does have some cash and has honored all of the existing loan covenants, however, it often makes sense to rework its loan instead of foreclosing and bringing the property to market.

Tales from the trenches

DuMars and his team are currently working on one case where a servicer has estimated that a retail center would sell at a loss of about 50 percent, if its loan were liquidated and the asset brought to market.

With the borrower offering to put in an additional $1.2 million of equity into the deal, the servicer deducted about 25 percent off the loan’s outstanding balance, minimizing the lender’s losses compared to liquidation.

Meanwhile, about $600,000 of the additional equity the borrower put into the deal will be used to re-tenant the property, and the remaining amount will be placed in interest reserve until the property is leased up.

The note holders in a case like that might not be thrilled, but “they are satisfied because everybody wins,” DuMars says. The trust makes out, because the net result is a return that would be a worth a few million dollars more than if the note were sold.

And the borrower benefits because he can continue to work on the project and try and increase its cash flow rather than having to walk away with a loss.

There are even some cases where special servicers are so reluctant to take properties back that they are willing to extend loans informally without asking for additional capital from borrowers.

Mason points to the example of one large shopping center in the New York metro region where the owner wanted to walk away from the property, but the servicer refused to take it back.

The center recently lost two big tenants to bankruptcy and could no longer pay debt-service coverage on its $90 million mortgage.

To keep the loan alive, the servicer instituted a cash-flow sweep, but has not modified the loan in any other way. No formal extension or modification agreement has been signed. Instead, month after month the servicer simply lets the borrower continue operating the property.

The reason the servicer is willing to remain in what Mason describes as a “Mexican standoff” is that it believes five years from now the property’s value will be equal to, or greater than, the value of the existing mortgage. The servicer wants to avoid selling the property today for less than the mortgage is worth.

“This is an extension by omission—they’ve extended the loan by not having done anything formally,” Mason says. “When loans get extended like that, nobody’s happy because it basically postpones the inevitable. But they are happier than seeing it foreclosed.”

The art of assumable debt

It seems that even when a workout is not possible, servicers are opting to keep the loans going in one way or another rather than liquidating.

Take for instance Metropolis Mall, a 409,815 sq. ft. property in Plainfield, Ind. Premier Properties USA Inc., the developer and owner of Metropolis Mall, liquidated in April 2009 and its mezzanine lender, Dominion Capital Management, gave up control of the property. The $86 million securitized first mortgage went into special servicing.

With the borrowing entity dissolved, the servicer in the case, Midland Loan Services, had no way to restructure the loan. But with the property facing some vacancy and rent issues, Midland didn’t want to bring Metropolis to market as is.

Instead, the servicer opted to keep the original loan in place and resize it, reportedly offering prospective buyers financing up to 95 percent loan-to-value. “The reason they are doing that is if the new buyer has to go for [outside] financing, the sales price is going to be lower,” Mason says.

When servicers offer assumable debt on a property, the sales price rises by an average of 15 percent, notes Margaret Caldwell, managing director of retail investment sales with the Atlanta office of real estate services firm Jones Lang LaSalle. She says that her group is currently at work on several transactions where the title to the loan will simply be transferred to the new buyer.