Despite the current financial turmoil and uncertainty in the markets, now is the time for fund managers to capitalize on distressed deal opportunities according to Ernst & Young’s Global Market Outlook: Trends in real estate private equity released last week.

Key findings of the report included:

- There will be a long, slow recovery in the real estate funds sector, but distressed deal opportunities will continue, and convergence of the bid-ask spread will foster greater deal volumes.

- Due to a wave of regulatory and financial reporting changes, the fund operating models will change over the medium to long term.

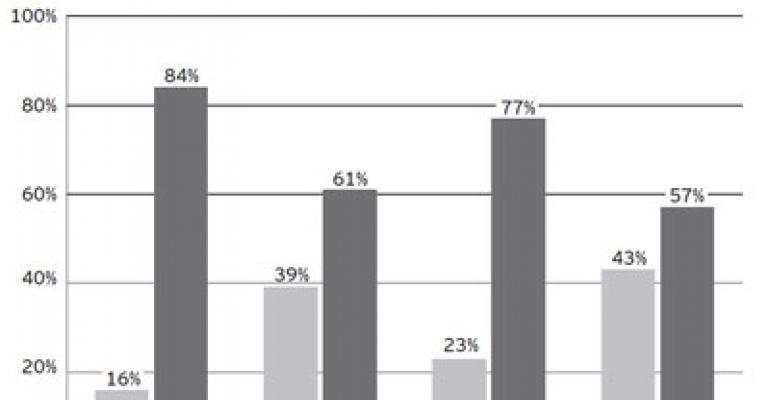

- Overall fund terms have not come back to where they were pre-crash, and many real estate fund managers have had to make investor concessions.

- Investors are now more focused on scrutinizing the real estate fund platforms where they are placing capital. More information will be needed to meet investors’ reporting requirements.

- For most fund managers, the fundraising process is significantly longer compared to predecessor funds.

- Fund managers required to register may find their marketability to investors improved.

“The market is considerably smaller than it was in 2007, and because it’s contracted so substantially, it may have now over-contracted,” Mark Grinis, Ernst & Young’s global real estate funds leader, said in a statement. “The market is much smaller in terms of the amount of equity being raised, the availability of debt financing and the number of transactions in the market. However, there are now signs the sector is reaching the bottom, and fund managers should brace themselves for an acceleration of deals and financing activity to hit the market, albeit slowly, over the next several years.”

One source of continued uncertainty is the changing regulatory and financial reporting environment that is being affected by the continued implementation of the Dodd-Frank Wall Street Reform and Consumer Protection Act domestically and the Basel III standards internationally.

In addition, the ways funds are being raised, expected returns, hold periods, exit strategies and handling of payouts have all changed post-crisis. For example, in 2007, most funds had waterfall payout structures that offered deal-by-deal returns. Today, there is an increasing trend “toward full pooling of returns as opposed to deal-by-deal returns,” according to the report.

Preferred returns have dropped slightly from 9 percent to 8.8 percent with target levered returns down from 20 percent or more pre-crisis to a range of 16 percent to 20 percent post-crisis. Average fund lives have also dropped from an average of eight years (with two one-year options) to six years. And overall leverage levels have dropped slightly as well from a range of 65 percent to 75 percent pre-crisis to 60 percent to 70 percent post-crisis.

The study included a survey of investors. One of the findings was that private equity real estate investors do not see REITs as encroaching on deals. According to the report, “Given that REITs were quite a success on both sides of the Atlantic in recapitalizing during the financial crisis, it seems that they are in a strong position to actively chase opportunities as they come to market. However, because of the difference in operating strategy and purchase criteria, they will generally be looking at core, core-plus and lower-risk assets.”