Apparel chains haven’t always been in the spotlight of regional mall line-ups. That starring role, and the job of generating mall foot traffic, traditionally rested on the shoulders of department stores. Specialty retailers just needed to focus on posting consistent sales growth, or they risked losing prime mall real estate to a competitor or a newer, fresher concept.

But now the retail industry is at a point where both department stores and specialty tenants are under pressure. All retailers, especially the fast-fashion retailers, are struggling to maintain the positive same-store sales growth that drives rents and makes for retail centers. The Gap has been closing stores. Aéropostale was pulled back from the brink of liquidation by a consortium of investors led by General Growth Properties and Simon Property Group, and is moving forward with a smaller store count.

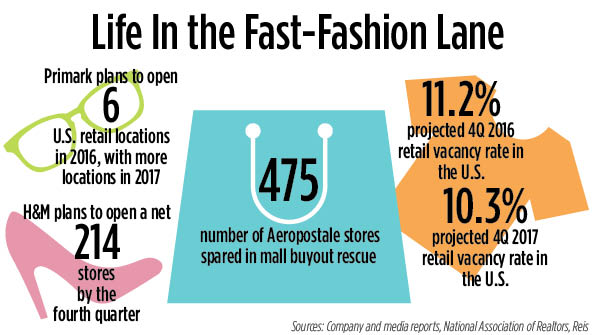

Now comes news that fast-fashion powerhouse H&M is beginning to experience weaker sales. The Swedish chain is one of the three most reliable fast-fashion retailers in the segment, a trio that includes Zara and Forever 21. However, recent news reports have claimed that Forever 21’s shipping firm had filed for bankruptcy and was cancelling its contract with the retailer because Forever 21’s business had dropped off sharply.

Then H&M, in its nine-month report, noted that it expected September sales to increase by just 1.0 percent, including the value-added tax (VAT). For a retailer accustomed to posting double-digit sales gains, including a reported a gain of 11.0 percent in September 2015, the news caused some market insiders to wonder whether H&M would begin to struggle with the same issues as its fast-fashion peers.

Millennial shoppers are not as brand-loyal as they have been in previous business cycles, and they are more fashion-forward, says Daniel J. Busch, a senior analyst with Green Street Advisors, a research firm based in Newport Beach, Calif. They do not care about quality as much as they do about staying on top of the next retail trend.

“The list of top mall tenants changes every 10 years or so and that is good,” says Busch. “Malls are adapting to the changing times.”

While consumer disenchantment and sluggish sales are bound to affect the fast-fashion segment, observers are already preparing for an industry with smaller footprints, and possibly more foreign operators.

Cutting a familiar business pattern

Until the industry settles into its new paradigm, retailers and landlords must deal with the realities of sluggish sales among national anchor brands and the continued impact of a growing e-commerce segment.

The latter is taking on even more urgency. Amazon.com has already launched seven in-house clothing lines. Online fast-fashion retailer ASOS, aimed at fashion-forward and value-conscious young adult shoppers, infuses its operations with a distinct social media feel, allowing its core 20-something constituency to browse and buy merchandise through its website and localized mobile apps.

Despite the challenges, regional malls continue to post solid property fundamentals. Data from the National Realtors Association and Reis shows that retail vacancy rates are expected to dip slightly to 11.2 percent in the fourth quarter of 2016, from 11.5 percent in the third quarter. Analysts at Green Street Advisors believe that non-anchor occupancy levels are still near peak levels.

Rent growth trends, however, are harder to ascertain for regional malls, because lease terms typically last five to seven years.

Fresher voices and perspectives

The fast-fashion segment is experiencing other positive developments, namely new entrants coming into the U.S. mall space. Primark, an Ireland-based discount fashion retailer, has begun opening stores in the U.S., with six locations slated for 2016. It has successfully positioned itself as a value clothing company, and has led some industry insiders to wonder whether the chain might be a good tenant fit for secondary, but stable, mall properties.

“The [customer] response is tremendous in Europe,” Busch says. “We will see how that plays out in the United States. It will be interesting to see how they fit into the mall merchandising mix.”

Six locations is merely a scratch on the retail landscape, but the retailer’s focus on value and its larger footprint might make it a candidate to help absorb vacancies left by the Gap, Aéropostale, PacSun and other specialty retailers that are either closing or scaling back.

Retail landlords will be waiting to see how the likes of Primark and ASOS impact the market. Hopefully, the companies will take more cautious measures for steady growth, according to Busch.

“A level of discipline is warranted in a big way,” he says. “There is a long list of retailers that have 800 stores [that] would rather have 300 or 400.”