It was the last minute rescue plan that few in the industry saw coming. Simon Property Group and General Growth Properties joined a consortium of other retail industry players to place a winning bid for the assets of bankrupt teen apparel chain Aeropostale, bringing the retailer back from the edge of an expected collapse.

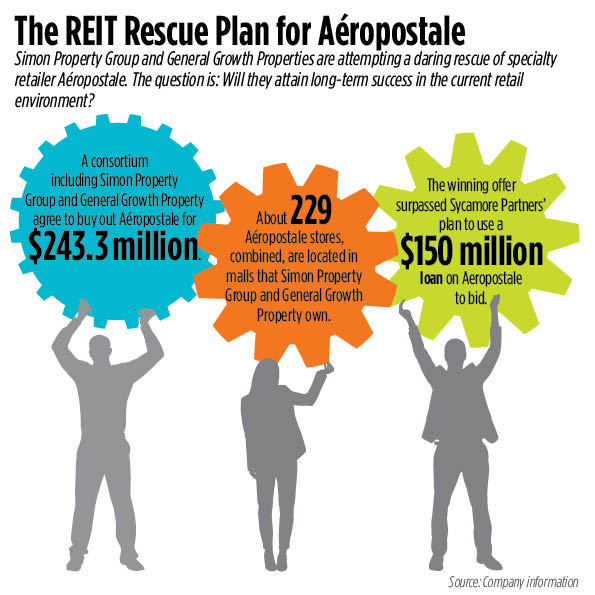

The New York-based company was facing liquidation early last week after a U.S. bankruptcy court ruled that private equity firm and Aeropostale creditor Sycamore Partners could use $150 million that the retailer owed it to bid for the company at auction. Simon and GGP combined resources with a group of seasoned retailing groups to submit a $234.2-million winning bid for the company last Thursday.

A rumored counterbid from Versa Capital Management never materialized, putting Aéropostale on the brink of liquidation. The consortium that eventually bought out the chain includes, in addition to the two mall REITs, Authentic Brands Group, a brand development and marketing firm; Gordon Brothers Retail Partners; a liquidator consultancy that also assists retailers with downsizings, acquisitions and other restructuring needs; and Hilco Merchant Resources; a specialist in retail asset monetization.

“Why would developers want to get involved in something like this? They’ve never done it before,” says Howard Davidowitz, chairman of Davidowitz & Associates, Inc., a national retail consulting and investment banking firm headquartered in New York City. “This is not their business, but they see the world crumbling around them.”

At no other time in the history of the retail industry have REITs made such a dramatic move to stop a tenant from going out of business. REITs have, however, partnered with struggling department stores in the past to carve out a mutually beneficial survival strategy. The closest example might be the joint venture that General Growth, Macerich and Simon formed with Seritage Growth Properties to own a combined 31 Sears Holdings properties, the latter’s spinoff REIT.

Mall and shopping center landlords have also established a track record of working out financial terms with restaurant operators to get spaces fitted out and operational, including fronting some of the set-up costs, says Melina Cordero, the head of retail research for real estate services firm CBRE. Restaurant tenants often agree to repay the landlord by paying higher rents or signing a percentage rent lease agreement, she notes.

Now that Simon and General Growth have intervened on Aéropostale’s behalf, the retailer has a new lease on life. The deal has also raised questions about whether mall landlords, who depend on specialty retailers and the rents they pay for survival, will begin to play a much more active role in helping retailers survive these turbulent times.

“It is about protecting their mall space and preventing vacancies and losses,” Cordero says. She adds that when a retailer files for bankruptcy, the resolution process is often long. During that time landlords do not often have a say in what happens to a space, even if they have a prospective tenant lined up to fill it.

“It is interesting,” Cordero says. “The landlords are stepping in to save themselves, more than anything.”

A changing relationship?

Like so many retailers lately, Aéropostale plans to close stores as part of its plan to stabilize operations and move toward profitability.

The Simon/GGP-led group intends to operate 229 Aéropostale stores, the retailer’s e-commerce business and the company’s international licensing business. If the retailer follows through on its plans that will likely put about 885 stores in North America, Puerto Rico and overseas up for closure and back onto the retail property market.

Aéropostale’s news developed just as Abercrombie & Fitch, another teen apparel retailer, reported that its second quarter same-store sales dropped by 7.0 percent. The company said that it expects same-store sales to remain challenged through the second half of the year, and that it might close 60 stores in 2016.

The relationship between landlords and tenants has traditionally been one where the former is the creditor, and the latter is obliged to perform well to hold onto its space. Davidowitz notes that while the market often looks to anchor store performance to assess the health of retail centers, specialty retailers pay most of the rent.

Landlords and restaurants have been developing a relationship akin to equity partners for years, and time will tell whether that will now extend to in-line tenants too, according to Cordero.

“Landlords and retailers are both trying to assert the place of brick-and-mortar in an omni-channel world,” Cordero says. “That is a fundamental change. We will all be watching to see what happens next.”