Real estate taxes, which are based on assessor opinions, are the only subjectively determined taxes on the planet. And unlike other building expenses, which are largely controllable, property taxes are volatile, chaotic and often quixotic. Above all else, in the District of Columbia, they are high.

So, how high are your property taxes? Presumably all owners can answer that question on a cost-per-square-foot basis. But there are other perspectives to consider. How much have those taxes changed in the past five years? What percentage of the property’s overall operating expenses do property taxes represent, and has that ratio altered over the years?

Here in D.C., we keep track of such things — and the results are startling. Office building taxes ballooned from $4.97 per sq. ft. in 2004 to $8.81 per sq. ft. in 2009, an increase of 77%. That’s more than double the rate of increase in office contract rents, which averaged $45.31 per sq. ft. in 2009, up 35% from $33.46 in 2004.

None of the tax increases in those five years resulted from changes in the millage rate, or tax per $1,000 of valuation, which remained essentially constant for the entire period. The increase was the product of assessment legerdemain, and would have been much higher had property owners failed to wage relentless and successful administrative and judicial tax appeals.

This pumping up of assessments allowed politicians the luxury of claiming that they did not raise the tax rate during the entire period. If taxes went up, even dramatically, well then that’s just the marketplace talking.

Never mind that the tax rate might have been significantly reduced, softening the blow of the assessment spikes, but it was not. After all, there were pet projects that needed feeding.

Economic toll

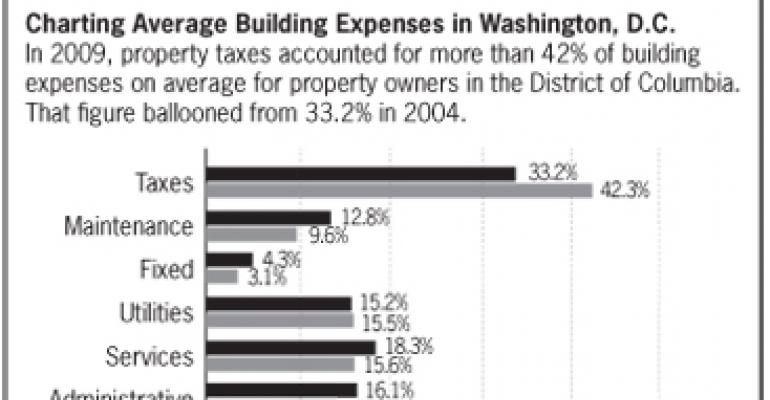

We can examine the impact of mushrooming assessed values on the bottom line. Non-tax building expenses including fixed costs, maintenance, utilities, administration and services rose modestly from 2004 through 2009, by perhaps 20%.

With tax bills growing at a faster rate, however, the tax burden as a percentage of total building costs increased dramatically over that same period.

By 2009, property taxes climbed to an astounding 42.25% of all operating expenses, up from 33.24% five years earlier. In the early 1990s, taxes were as low as 24% of all operating expenses.

The overall effect on property cash flow was to significantly blunt the profitability one might have expected from the general rise in property values over the period.

Let's examine that further. Average rental rates increased 35% over a five-year period. If property taxes had increased at the same rate, taxes on the average office building would be $6.71 per sq. ft.

But because property taxes actually climbed 77% over that five years, the average office taxes is $8.81 per sq. ft. That's $2.10 per sq. ft. lost from the bottom line.

In a 250,000 sq. ft. office building, not uncommon in D.C., that equates to a loss of $525,000, annually.

Let's now look at it from the perspective of the taxing authority. There are approximately 1,000 privately owned office buildings in D.C. If the average size were, say, 175,000 sq. ft., D.C. arguably would be gaining excess tax revenues approaching $400 million annually.

That is a staggering sum, a massive shift of the tax burden heaped quietly onto the shoulders of commercial owners.

The D.C. government, always a minority partner in real estate enterprises, has been biting off heftier chunks of the commercial pie through taxation as the years roll by.

This has allowed it to subsidize homeowners (i.e. voters) through reduced tax rates and capped increases. And everybody’s happy. Oh, except commercial owners and their tenants, the geese that lay the golden eggs. And we all remember what happened to them.

A proposal

Over the years, commercial owners have raised many salient arguments in an attempt to hold down their taxes. For example, commercial taxes in D.C. are considerably higher than in the adjacent jurisdictions, suburban Maryland and Virginia, resulting in a competitive disadvantage for D.C. property owners.

Arguing this point has brought some success in lowering the D.C. tax rate, but a large disparity remains.

Most recently, recalcitrant D.C. assessors were slow to recognize the downturn in the economy that afflicted property values in all jurisdictions. When the economy improves, aggressive assessors will tend to be overzealous in pursuing and overstating the market.

Simply put, property taxes shouldn’t increase at a faster rate than rents. In practice, such a rule would require first establishing a base line of rents and taxes, and then utilizing reliable data to establish increases.

There might be lag time involved in acquiring and utilizing the data, but that challenge is a hill, not a mountain, to climb. And most importantly, it would be reasonable and fair.

Stanley J. Fineman is a shareholder in the law firm of Wilkes Artis Chartered, the District of Columbia member of American Property Tax Counsel. He can be reached at [email protected].