After several quarters with flat to improving fundamentals, real estate research firm Reis Inc.’s latest report showed a spike in the regional mall vacancy rate to a new peak. The rate at shopping centers, meanwhile, remained flat.

The firm originally reported the findings in early April before issuing its Retail First Glance report on Friday. The report serves as a pre-release analysis of its quarterly retail report.

The vacancy rate at malls reached 9.1 percent—a 40 basis point jump from the previous quarter. As a result, the vacancy rate surpassed the previous high of 9.0 percent reached in the second quarter of 2010. The rate had declined in the third and fourth quarters of last year before the recent jump. The figure is the highest since Reis began tracking the sector in 2000.

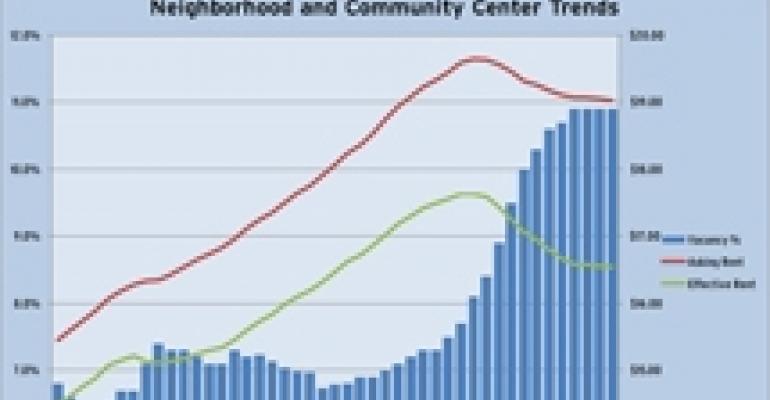

On the neighborhood and community center front, the vacancy rate remained stable at 10.9 percent—the same figure as in each of the previous three quarters. It remains at its highest level since an all-time peak of 11.1 percent in 1990.

In the company’s monthly commentary Reis Senior Economist Ryan Severino wrote that there are still reasons to be worried about the outlook for both regional malls and neighborhood and community centers.

According to the report, “The main reason why [neighborhood and community center] vacancies have trended flat is because inventory growth has slowed to a crawl. Only 83,000 square feet of new neighborhood and community center space came online this period, the lowest level of new deliveries for any quarter since Reis began publishing quarterly data in 1999. With such constrained supply, a market on the way to recovery would have posted vacancy declines from rising demand. It appears there is no such rising demand for retail space, at least for the near term. In other words, flat vacancies represent the absence of demand more than a sector heading for recovery. Asking and effective rents continued to decline, both by 0.1 percent this quarter, reflecting continuing weakness in pricing power on the part of landlords.”

The vacancy rate for neighborhood and community centers remained flat or declined in 26 of the primary 80 metropolitan areas while effective rents remained flat or declined in 45 out of 80 markets. “These trends reflect broader national figures, and augur for a continuing bumpy road ahead for retail properties,” Severino wrote. “With the absence of demand for new retail space, any new property that comes online will find it difficult to find new tenants.”

Regional mall malaise

In addition to the decline in vacancies, asking rents at malls also fell by 0.1 percent in the first quarter, almost negating the increases posted by the sector late last year. Rents now stand where they did in the second quarter of 2006.

According to the report, “Large blocks of space went vacant from January through March in a number of properties, several from tenants that had given word earlier in 2010 that they were scaling back or vacating their occupied spots entirely. In line with the overall theme of the lack of demand for retail space, even regional malls do not appear to be immune from hiccups on the path to recovery. Not coincidentally, a lot of the space that went vacant came from properties which lost an anchor tenant in 2009 or 2010. What we’re seeing appears to be echo effects of malls having lost anchor tenants in the last downturn – now we’re seeing blocks of non-anchor tenants, or other anchor tenants, giving up their leases. This was likely due to a decline in foot traffic at these anchorless centers and to the cotenancy clauses that often give inline tenants the option to break their lease without penalty if the anchor spaces are vacated and not released within a stated period of time.”

Overall, Reis remains worried about consumer demand--in contrast with a more bullish outlook published the same day by Hessam Nadji, managing director of research services with Marcus & Millichap Real Estate Investment Services.

Nadji—comparing store-based retail sales with net absorption trends—concluded that the industry should expect more store openings in the coming months.

Nadji wrote, “Historically, surges in store-based retail sales have triggered an expansion cycle by retailers. Given the strength of recent retail activity, an accelerated pace of expansion will likely ensue once confidence in the sustainability of the recovery overrides caution.”

For its part, Marcus & Millichap found that retail property vacancy nationally stood at 10.0 percent in the first quarter—unchanged from the previous quarter and down 30 basis points year-over-year. It expects increased demand to generate 93 million square feet of net absorption nationwide, which will push the national retail vacancy rate down to 8.5 percent while asking rents will rise 1.2 percent and effective rents will rise 1.8 percent.

Severino, however, wrote, “Although the economy has been growing for the last 6-7 quarters and the labor market has been improving for the past year, the recovery has not been strong enough to translate into increased consumer demand in any meaningful fashion. While the increase in retail sales is heartening news for landlords, it is important to remember that this is growth from a very low base because retail sales plummeted during the recession. Until the labor market mounts a more meaningful recovery, retail sales growth will remain below the level sufficient for increasing tenant demand for retail space.”

Reis expects 9 million square feet of new shopping and community center space to come online in 2011, roughly double the figure for 2010, which it expects will result in vacancies for that segment beyond the record 11.1 percent reached in 1990.

As a result, Severino concluded, “In stark contrast to strong recoveries from multifamily buildings, and a dip in vacancy for office properties, expect another difficult year for retail properties in 2011.”