Fundamentals continued to improve for regional mall REITs during the second quarter of 2010, leading analysts to conclude that the sector had largely shaken off the aftereffects of the recession.

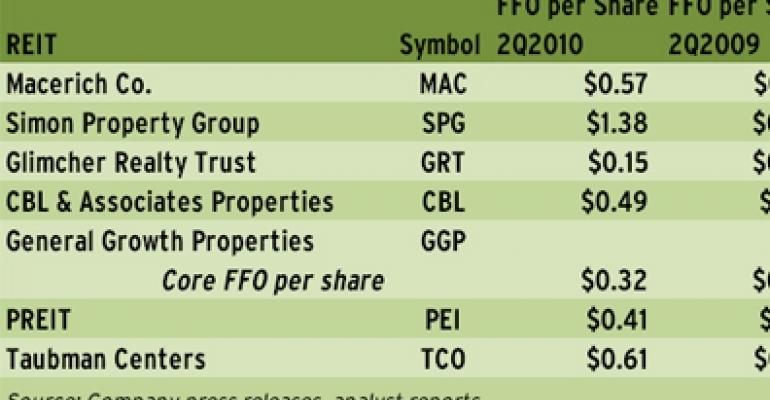

For the three months ended June 30, three regional mall REITs beat consensus analyst estimates on FFO per share and two were in line with expectations. Only Santa Monica, Calif.-based Macerich Co. (NYSE: MAC) missed estimates, by $0.04 per share. The miss was due primarily to higher than expected interest expense and lower than expected income from joint ventures, according to Rich Moore, REIT analyst with RBC Capital Markets.

Indianapolis-based Simon Property Group (NYSE: SPG), Chattanooga, Tenn.-based CBL & Associates Properties (NYSE: CBL) and Bloomfield Hills, Mich.-based Taubman Centers Inc. (NYSE: TCO) beat estimates by a range of $0.02 per share to $0.05 per share. Columbus, Ohio-based Glimcher Realty Trust (NYSE: GRT) and Philadelphia-based Pennsylvania Real Estate Investment Trust (PREIT) (NYSE: PEI) met analysts’ expectations.

Even more encouragingly, Simon, Macerich and Glimcher reported rising same-store NOIs in the second quarter, ranging from a 0.4 percent increase for Glimcher to a 2 percent increase for Macerich. Regional mall REIT executives reported seeing a strong resurgence in leasing interest from tenants, which has pushed up leasing velocity in the past few months.

“I think you have seen [leasing] volumes pick up. And I am not calling it robust, but the retailers are making money, they’re talking, they are clearly coming to the realization that the supply of rate centers is limited,” said Macerich chairman and CEO Art Coppola during the company’s conference call with analysts on Aug. 9.

In addition to retailers’ improved financial situation, the lack of new development on the horizon might be helping the sector recover faster than previously anticipated, according to Moore. Most retail REITs continue to focus on redeveloping existing centers, and are not expected to start new construction in 2010. Meanwhile, the supply of existing quality mall space is scarce enough that some retailers are having difficulty meeting their opening plans for 2011, Moore notes.

In the second quarter, portfolio occupancies for Simon, Macerich, Glimcher, Taubman, PREIT and General Growth Properties (NYSE: GGP) stood above 90 percent. CBL & Associates reported occupancy of 89.6 percent.

In spite of across-the-board increases in tenant sales, however, rents continued to decline. At Glimcher properties, for example, average rent per square foot slipped 0.7 percent to $26.82, from $27.01 in the second quarter of 2009. REIT executives have been trying to counteract this trend with shorter lease terms, according to Jason Lail, senior real estate analyst with SNL Financial, a Charlottesville, Va.-based research firm.

“With this, regional malls have positioned themselves as being able to increase rents in a shorter time period if employment and the economy continue to improve,” Lail says. “While tenants also have the ability to leave assets earlier than normal with these shortened lease lengths, overall they have been a good method for maintaining short-term upward movement in lease pricing.”

Lail cautions, however, that high unemployment continues to be a major concern for the regional mall sector, as job growth is tied to discretionary spending. In July, the national unemployment rate remained unchanged from the month prior, at 9.5 percent.