Commercial real estate professionals have been wondering how the market would deal with the wave of commercial mortgage debt maturing in the next year and a half, particularly at a time when lending standards are considerably more conservative than they were 10 years ago.

Last week, the market got an indication of the consequences that lay ahead for the retail sector, after General Growth Properties defaulted on a $144 million mortgage on the Lakeside Mall, a 1.5-million-sq.-ft. retail center in Sterling Heights, Mich., a suburb of Detroit.

“Right now, the mortgage is too high for the retail lending environment,” says Alex Goldfarb, a senior REIT analyst at Sandler O’Neill + Partners.

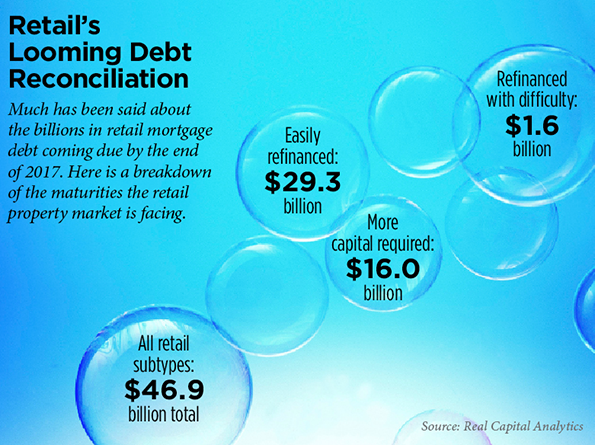

Debts like the one attached to Lakeside Mall can potentially be managed without weakening the financial position of other shopping centers in General Growth’s portfolio or threatening the company’s overall health. The larger issue is how the retail sector will manage the CMBS loans coming due by the end of 2017. The amount of CMBS retail debt outstanding is an estimated $47 billion, according to Real Capital Analytics, a New York City-based research firm. The question is even more urgent in the case of class-B malls anchored by department stores and specialty retailers struggling to maintain foot traffic and healthy same-store sales.

“If it is a mall where they think there is future potential, they could work to restructure [the mortgage],” Goldfarb says, adding that: “The world is going toward the more dominant retail center.”

So while General Growth might work out a solution for the Lakeside Mall mortgage, the industry overall has to grapple with a lending environment that it tighter than it was 10 years ago.

Lagging behind the curve

Even if Lakeside Mall’s loan-to-value ratio conformed to the existing range of 60 percent to 65 percent, traditional sources of financing are pulling back. Activity in the CMBS market has ebbed. Local and regional banks are facing new regulations that would reign in the companies’ willingness to extend commercial real estate loans.

Property prices in the shopping center sub-sector haven’t rebounded to the levels seen before the financial crisis, a situation that might complicate the refinancing process, if General Growth chooses that option. Retail real estate prices hit a peak in August 2007, then slid a cumulative 42 percent three years later, according to the RCA report, “Finding Opportunities in Distressed Retail Mortgages.”

“Prices overall are still 12 percent below that previous peak level,” says Jim Costello, a senior vice president with RCA. “Back then, mortgages had an average loan-to-value ratio of 70 percent. Some of the most high-profile defaults that everybody points a finger at had more leverage than 70 percent.”

Despite the lag in prices, Costello expects landlords to work out solutions to their overleveraged properties. Of the outstanding maturities in the retail sector, about $29.3 billion could be easily refinanced, according to the firm.

“There will not be a surge of REO activity across the board from this,” Costello says.

Room for reasonable doubts

To be sure, General Growth’s default on Lakeside Mall still poses potentially serious implications for the market, and not just because the REIT is one of the largest mall developers in the industry. It unfolded amid a cluster of other significant developments in the sector. Starwood Capital Group is said to be planning to sell off $1.2 billion worth of properties that the company bought from Westfield Properties, according to Bloomberg.

On June 20, WP Glimcher announced a major shake-up in its leadership and corporate structure. Michael P. Glimcher resigned as vice chairman, CEO and director of the company. Louis G. Conforti became interim CEO, and Robert J. Laikin stepped in as the non-executive chairman of the board. The company also restructured its board of directors, and plans to restore the company’s name to Washington Prime Group. The moves undid a partnership that Washington Prime Group put into place when it purchased Glimcher Realty in a deal worth about $4.3 billion.

The moves also suggest that Washington Prime might trim its portfolio, potentially delaying the recovery in retail property prices.

“During the next few months, the focus is straightforward: maximize current cash flow of the company which involves traditional and innovative leasing as well as reducing [general and accounting expenses],” Conforti said in a company statement. “In addition, an evaluation as it relates to the company’s portfolio composition is to be undertaken.”