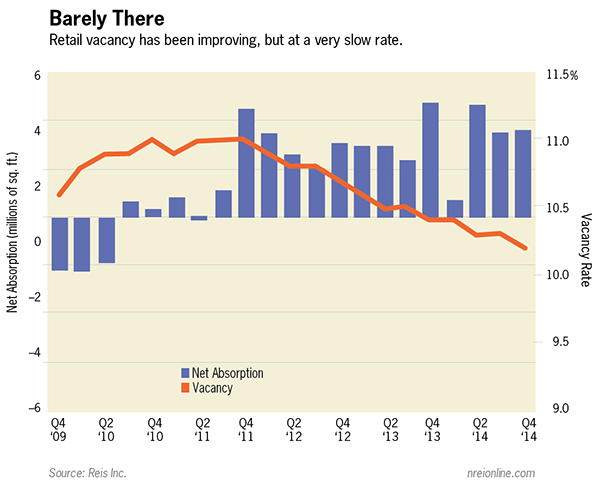

Improvements in the retail sector in the fourth quarter were once again tepid. The national vacancy rate for neighborhood and community centers declined by just 10 basis points, to 10.2 percent, a slight improvement from the third quarter when vacancy remained unchanged. For full-year 2014, vacancy declined by just 20 basis points. National vacancy is now down 90 basis points from its historical peak during the third quarter of 2011, representing an improvement of less than 10 basis points per quarter. This is an incredibly meager amount by historical standards, and is indicative of the headwinds that this property type continues to face.

New construction remains limited, with completions totaling just 1.8 million sq. ft. Very few new centers are being built and most of the construction is in the form of expansions to existing centers. Financing is still strictly tied to pre-leasing requirements, which is limiting the market. Moreover, fundamentals are just too weak to create much incentive for new development, outside of a handful of projects. Demand for existing inventory will increase in the coming years as the economy and labor market continue to recover, but we have yet to move beyond the nascent stages of a recovery in demand for retail space.

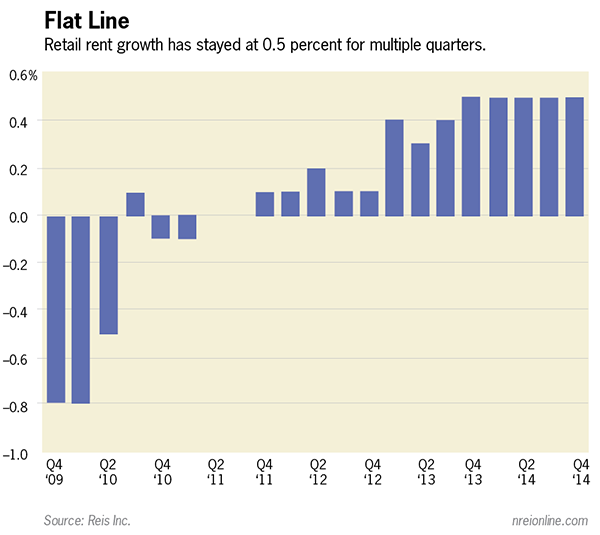

Asking and effective rents both grew by 0.5 percent during the fourth quarter. Rent growth has been stuck at a 0.4 percent—0.5 percent quarterly pace, providing further evidence that the recovery is not yet accelerating. Although rents have been growing since the fourth quarter of 2011, effective rents remain roughly 2.5 percent below peak levels from before the downturn six years ago. During 2014, asking and effective rents expanded by 1.8 percent and 2.0 percent respectively, roughly the rate of inflation. Though tepid, that is the fastest rent growth in the market since 2007, reinforcing what a tough slog this has been for retail centers. The slow, but steady declines in vacancy will eventually translate into greater rent increases, but that is not likely to occur in the near term.

Mall vacancy increases

During the fourth quarter, regional mall vacancy increased by 10 basis points to 8.0 percent. This is the first quarterly increase in the mall vacancy rate since the third quarter of 2011. For full-year 2014, the mall vacancy rate was also up 10 basis points. The primary culprit was the closing of a number of Sears stores during the fourth quarter. Based on recent announcements from retailers such as J.C. Penney, Macy’s, Izod, and Wet Seal, the mall sub-sector is not done with store closings yet. Although the market recovery had been losing steam before this, with the national vacancy rate flat for most of 2014, this will likely cause more short-term disruptions for the mall sub-sector.

While there is no new construction in the mall sub-sector save expansions of existing malls, demand for space should increase along with the recovery in the economy and labor markets in 2015, even while owners deal with the fallout from ongoing store closures. However, any improvement in demand will come from average-caliber malls, class-A-minus and below. Vacancy at high-end class-A and better malls has just about vanished, giving landlords strong pricing power, but little ability to increase net operating incomes (NOI) due to occupancy changes. Vacancy at average malls remains relatively high and still has significant room to compress over the next few years as the economy grows and consumer spending increases.

Structural, not cyclical?

Most recent macroeconomic data portends better times ahead for retail in 2015 and beyond. This is especially true of the labor market where the pace of job creation has accelerated. Moreover, cheaper energy prices should buttress the retail sector by increasing consumers’ disposable income. There is typically a six-month lag between declines in energy prices and an uptick in retail sales. Given that the decline in energy prices began in mid-2014, we are likely on the precipice of improved retail sales performance in the first half of 2015. That could potentially spur the retail sector into a somewhat faster recovery than we were anticipating before the precipitous decline in oil prices. While we are still a number of years away from characterizing the retail real estate environment as "strong," 2015 could certainly be a year of transition to a healthier market.

Despite the economic tailwinds, retail data increasingly shows that a structural shift is occurring in the property type. A proliferation of relatively new retail sub-types has occurred over the last 15-20 years. The rise of lifestyle centers, town centers, power centers and, more recently, outlet centers, is undoubtedly siphoning demand away from neighborhood and community centers and even some weaker malls. For example, the vacancy rate for neighborhood and community shopping centers has barely budged over the last few years as consumer spending has recovered. Meanwhile, the vacancy rates for class-A malls are at historically low levels, while vacancy for power centers is nearing pre-recession levels. The downturn has likely exacerbated the trend away from neighborhood and community centers.

The rise of e-commerce has also been a major contributor to this shift. The continued blurring of the lines between “bricks” and “clicks” and the continued focus on consumers’ experience with products, both in and out of stores, will continue to cause disruption in the retail market, rendering some traditional neighborhood and community centers somewhat obsolete. Centers at the heart of communities, especially those with grocery anchors, are not going away anytime soon. However, for the majority of that retail sub-type, the best days are likely in the past and not the future. Therefore, even as we anticipate a recovery, we should likely not expect vacancy rates to reach levels seen before the downturn.