Shopping center REITs continued to make headway in re-leasing vacant big box stores in the first quarter, leading to stable occupancies and smaller declines in same-store NOIs compared to 2009. Like their counterparts in the regional mall sector, however, shopping center REITs still struggled with weak rental rates on leases negotiated in prior quarters.

“In the shopping sector, the [REITs’ performance] was encouraging,” says Rich Moore, an analyst with RBC Capital Markets. “For the first time in a long time I’ve heard these guys say that retailers are telling them there is not enough good space left for store openings in 2012.”

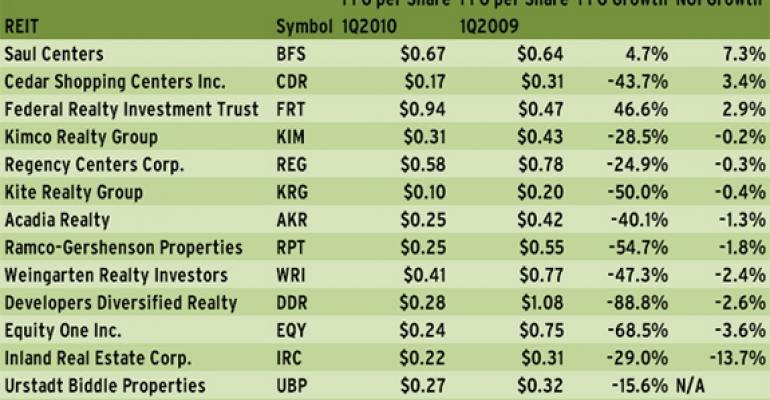

For the quarter ended March 31, four shopping center REITs met consensus analyst estimates for FFO per share, three were in line with expectations and four missed. Kimco Realty Corp. (NYSE: KIM), Regency Centers Corp. (NYSE: REG), Federal Realty Investment Trust (NYSE: FRT) and Saul Centers Inc. (NYSE: BFS) beat analyst estimates by a range of $0.01 per share to $0.08 per share.

Ramco-Gershenson Properties Trust (NYSE: RPT), Cedar Shopping Centers Inc. (NYSE: CDR), Kite Realty Group (NYSE: KRG), Weingarten Realty (NYSE: WRI), Urstadt Biddle Properties (NYSE: UBA) and Equity One Inc. (NYSE: EQY Developers Diversified Realty (NYSE: DDR), Acadia Realty Trust (NYSE: AKR) and Inland Real Estate Corp. (NYSE: IRC) met analyst expectations.

A few of the stronger players, including Federal Realty Investment Trust and Saul Centers, posted healthy NOI increases in the first quarter (in Saul’s case, the increase was largely due to collection of past due charges from a former anchor tenant). The remaining REITs posted some of the smaller NOI decreases in many quarters. The exception was Inland Real Estate Corp., which posted a 13.7 percent decrease in same-store NOI, which the firm’s executives attributed to previously announced retailer bankruptcies and lease terminations. Inland’s portfolio occupancy fell 140 basis points compared to the first quarter of 2009, to 92.2 percent.

Nevertheless, during the REIT’s May 4th earnings call with analysts, Inland president and CEO Mark Zalatoris noted the firm was making progress in re-leasing many of the vacant big boxes in its portfolio.

“Including leases signed during the quarter, we have re-leased 74 percent of the vacancy created by the bankruptcies of Vicks, Linens ‘n Things, Circuit City, Bally’s Fitness and Filene’s Basement,” Zalatoris said. “Another 17 percent of that vacancy is at least under letters of intent.”

Many of Zalatoris’ colleagues in the shopping center sector confirmed that leasing conditions were improving, though rental rates still left something to be desired. The sector will likely see better results in the third and fourth quarters of 2010, as retailers try to plan the opening of new stores for the back-to-school and holiday shopping seasons, according to comments made by Daniel B. Hurwitz, president and CEO of Developers Diversified Realty, during the company’s Apr. 23rd earnings call.

“We are encouraged by the aggressiveness we are seeing with some of our stronger retail partners,” he noted.