With an optimistic outlook on leasing and freshly scrubbed balance sheets, regional mall REITs ended the first quarter on a healthy note, according to analysts.

During the quarter, sales per square foot and occupancy levels both improved. Rental rates, however, remained a lingering weakness. REIT executives attributed the stagnant rental rates to the fact that many leases completed this year were negotiated in the third and fourth quarters of 2009, when tenants were still seeking breaks. But a recent surge in interest from tenants has analysts predicting that regional mall REITs’ rental rates might recover faster than rents in the broader market.

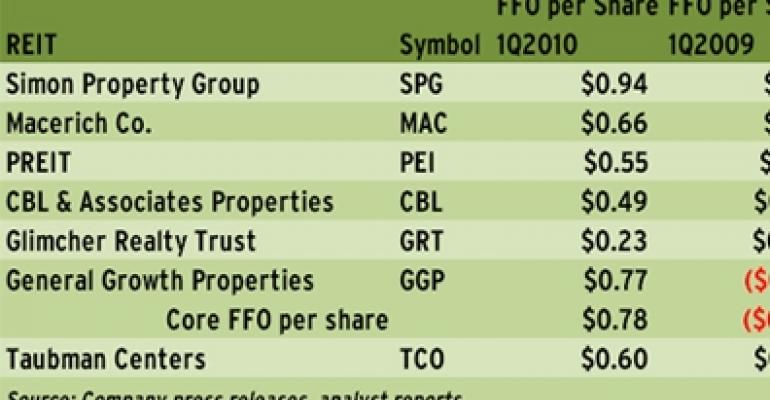

Of the seven regional mall REITs, four beat consensus analyst FFO estimates for the quarter ended March 31, by a margin of $0.02 per share to $0.10 per share. The outperformers included Simon Property Group (NYSE: SPG), CBL & Associates Properties Inc. (NYSE: CBL), Glimcher Realty Trust (NYSE: GRT) and Pennsylvania Real Estate Investment Trust (PREIT) (NYSE: PEI). Two companies, Macerich Co. (NYSE: MAC) and Taubman Centers Inc. (NYSE: TCO), missed consensus estimates, by $0.02 per share and $0.04 per share respectively. Analysts do not currently provide estimates for General Growth Properties (NYSE: GGP).

The widespread declines in year-over-year FFO comparisons in the first quarter, which affected every firm except General Growth, could be explained by the REITs’ recent stock offerings, which had been undertaken to reduce debt and prepare the companies for potential future acquisitions, according to Robert McMillan, a REIT analyst with New York City-based Standard & Poor’s Equity Research. Companies including Macerich and PREIT have conducted common stock offerings this spring.

“From a balance sheet perspective, a lot of companies are now better positioned and less risky,” says McMillan.

According to research from RBC Capital Markets, only Glimcher and CBL currently have debt-to-market-capitalization ratios greater than 50 percent.

Operating metrics have also improved noticeably in the first quarter, with Simon, Macerich and PREIT reporting modest increases in same-store NOIs. The remaining REITs reported smaller NOI decreases than in previous quarters. With tenants seeing improved sales, leasing activity has picked up in recent months, REIT executives note. The catch is that with the lingering weakness in rental rates, the REITs have been signing leases for two- and three-year terms instead of the standard five- to 10-year leases.

As the year progresses and the amount of available class-A space at regional malls shrinks, retailers will likely become more open to signing deals at higher rents, notes Rich Moore, an analyst with RBC Capital Markets. He notes that for the REITs, rental rates on new deals will likely rise before the end of the year, ahead of the general market.

“The amount of deals they are doing is very strong—that’s the first step in getting to the point where you are getting some [rent] recovery from tenants,” Moore says.

—Elaine Misonzhnik